This article is part of an occasional series by Geoff Tily on real interest rates – see also Do real interest rates follow ‘historic norms’?

The Bank of England have just updated their incredibly useful historic data resource, not only adding another six years of figures to 2015 but also expanding greatly the range of information included.

Of particular interest is a measure of UK corporate interest rates that extends back to the mid-1840s (compiled from a variety of sources). Using the Bank’s GDP deflator series, a measure of real interest rates can be derived and is shown below.

Figure 1:

Rates are averaged (green lines) over episodes based on changes in (my interpretation of) policy doctrine as follows:

A. Dear money under financial liberalisation and gold standard exchange regime of the 1920s

= 6.5%.

(The figures vindicate Keynes’s June 1931 judgement: “The leading characteristic [since 1924] was an extraordinary willingness to borrow money for the purposes of new real investment at very high rates of interest – rates of interest which were extravagantly high on pre-war standards, rates of interest which have never in the history of the world been earned, I should say, over a period of years over the average of enterprise as a whole. This was a phenomenon which was apparent not, indeed, over the whole world but over a very large part of it” – lecture to the Harris Foundation in Chicago, Collected Writings, Volume XIII, pp. 343–5.)

B. The cheap money policy from 1932 until the end of the war

= 0.3%.

C. Lower rates through the golden age of economic activity under the Bretton Woods regime (1945-1970)

= 1.7%

(Though really two distinct periods are apparent: discussed further below.)

D. Negative real rates resulting from the 1970s inflation

= – 1.0%

E. Dear money under the second financial liberalisation of the twentieth century

= 5.6%

F. Reduced interest rates since the turn of the millennium

=3.2%

The only precedent to the dear rates of the second financial liberalisation are those of the first liberalisation in the 1920s, which Keynes warned should be avoided “as we would hell-fire”.

In a contribution earlier this year Gene Kindberg-Hanlon of the Bank of England argued that real interest rates had returned to long-term norms. Strikingly real rates since the turn of the millennium are the same to one decimal place as those that prevailed for the sixty years before the First World War. But it is a tall order to regard the trajectory for the 90 years in-between as an adjustment process. Instead movements in interest reflect fundamental shifts in policy.

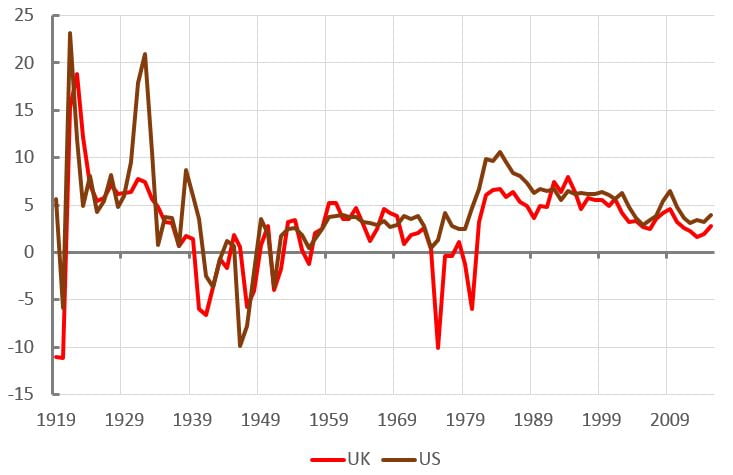

Up until now the only readily available (as far as I have been aware) long-term corporate interest rates have been for the US (via the Federal Reserve). Comparing the two sets of figures suggests, unsurprisingly, that shifts in policy operate on a global basis, though with some national differences. Most notably US rates were higher in the great depression as a result of the more severe price deflation. Conversely US rates remained positive in the 1970s, with inflation less severe than in the UK.

Figure 2: UK and US long-term corporate real rates of interest

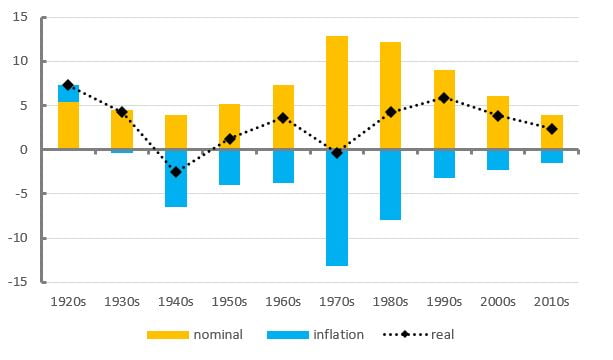

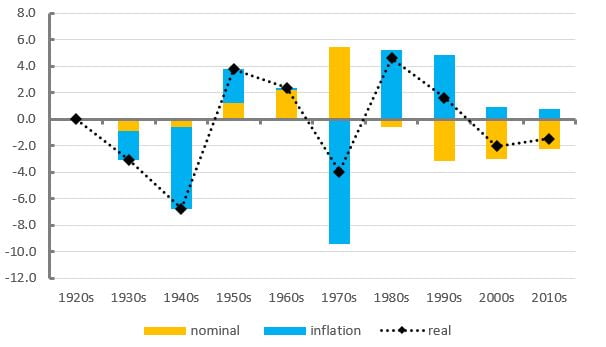

Movements can be examined in more detail by decomposing real rates into nominal rates and price change. For clarity figure 3 shows the decomposition by decade (inflation is shown with a negative sign), and figure 4 shows decade to decade change. (R is nominal rate; P is inflation and r the real rate.)

Over the period of Keynes’s greatest influence on monetary policy, both nominal and real rates fell into the 1930 and 1940s. From the 1950s nominal rates began to drift upwards, with lower rates of inflation also supporting higher real rates. From the 1960s, the sum of the parts was considerably higher real rates. I hadn’t fully internalised the scale and abruptness of this increase before, with the match with US annual figures into 1959 re-enforcing the point – perhaps this followed from the Eurodollar market being allowed to take root and the inherent capitulation to financial power?

Figure 3: UK real interest rates by decade, percentage points

Figure 4: Change in UK real interest rates by decade, percentage points

Then in the 1970s real rates collapsed because of high inflation.

For the next two decades real interest rates were at a very high level, with nominal rates kept much higher relative to falling inflation. In the twenty-first century real rates fell as reductions in nominal rates outstripped falling inflation. But there should be no pretending that the end position constitutes cheap money.

Post-script: I leave aside the economic consequences of playing again with hell-fire, but see e.g. here.