The Fabian Society invited Nicola Smith of the TUC, Dan Corry – once a Labour government adviser – and me to address their Summer Conference last Saturday. The theme: how can Labour restore its economic credibility with the electorate? The audience was large – about 300 earnest, well-informed and assertive Fabians. The discussion was lively, with a buzz, as the session immediately following was to be a hustings for Labour leadership candidates.

The need for the biggest British opposition party to restore a degree of economic credibility is urgent – both in its own interests, but also in the public interest. But it will be tough, with little help expected from a majority of the economics profession.

Economists are divided into two camps, with microeconomists – those who specialize in the branch of economics that analyses the market behavior of individual consumers and firms – the dominant majority within academia and amongst economic commentators.

As a result, in discussing the economy as a whole, most economists tend to draw macroeconomic conclusions from microeconomic reasoning. In other words they tend to extrapolate from the experience of an individual, household or firm – to government and the wider economy. Like George Osborne they discuss the government’s finances as if the government can be compared to a household.

This has confused the electorate (not to mention politicians) which rightly believes that households should “live within their means”, “balance their budgets” and “eliminate their deficits”. (Although of course, many households, with both assets and a relatively secure income, make sensible long-term investments in for example, a home. We do so by borrowing large sums long-term.)

But governments do not operate as households do, as explained below. This has not prevented the Chancellor from pretending that government can. He’s so determined to maintain this flawed, and blatantly ideological narrative: and members of the opposition Labour Party are so eager to echo the narrative, that I feel it only right to rehearse the opposing arguments again…and again.

So as a guide to a series of rebuttals, I will reference the Chancellor’s recent speeches – including one delivered on 20 May, 2015 to the CBI.

1. “We’re going to ….eliminate the deficit”

Despite his five year experience of failing to “eliminate the deficit” the Chancellor had this to say on 20th May, 2015:

“So in this Parliament we’re .. going to deal with our debts and eliminate the deficit….. fixing the public finances so our country lives within its means”

What’s the problem with this statement from the man at the top of a department – the Treasury – that boasts some of the cleverest economists in the country?

Just this: no matter how determined he may be, the Chancellor cannot eliminate the deficit – the balance between government income and expenditure.

While you and I can cut our overdrafts by cutting our spending, or by increasing our income – the all-mighty Chancellor cannot do the same. The public sector deficit is not dependent on his actions, or the government’s policies. It is dependent on economic activity in the economy as a whole. If the economic ‘cake’ (that is employment) shrinks, the government deficit will rise. As the ‘cake’ expands, the government deficit will fall.

The OBR puts it well:

“Movements in the budget deficit are in part the result of the ups and downs of the economy. When the economy is strong, the deficit will be lower as taxes flow in and welfare costs are reduced. The opposite is true when the economy is weak.”

The budget deficit is an outcome – of decisions made by both the private and public sectors to expand or contract activity; of the levels of both public and private employment; of the amount collected in tax revenues.

However while the Chancellor can’t “eliminate the deficit” he can cut government expenditure and investment. Or increase government expenditure and investment.

In other words, it is not possible to assess the stance of the Chancellor’s fiscal policy from estimates of the public sector deficit – the outcome. But an expansionary fiscal policy can lead to growth in activity and employment, so that, in a recession, public sector expenditure and investment creates employment, generates tax revenues, saves on benefits and welfare payments and thereby reduces the deficit.

A policy of fiscal consolidation or contraction, at a time when the private sector is in a slump, suffering from an overhang of debt, weak productivity, a lack of confidence and is hoarding cash and withholding investment, will cause the deficit to rise.

So the debate is not between those who would “slash the deficit” and those who would “postpone” the reduction in the deficit.

Instead the debate is between those who would cut expenditure and investment in a slump, as opposed to those who would stimulate public expenditure and investment at times of private sector weakness.

Mr Osborne knows full well, and from bitter experience that he cannot cut the deficit. As Business Insider notes: “the government’s June 2010 projections forecast that the budget would be balanced by 2014/15, the fiscal year just gone.” But that was not to be. Despite substantial cuts to government spending, “the [OBR’s] March 2015 outlook put the 2014-15 deficit at 3.3% of GDP.” That’s a lot of red ink. The Office for Budget Responsibility expects the deficit to be about £75 billion in 2015-16 in total, or £46 billion excluding investment borrowing.[1]

It gets worse. Contrary to Mr Osborne’s fervent hopes and promises, the OBR expects UK public sector net debt to peak relative to the size of the economy in 2014-15 at 80.4% of national income – the highest ratio since the late 1960s. (Net debt, the OBR notes, was less than 40 per cent of national income prior to the slump that followed the financial crisis.)

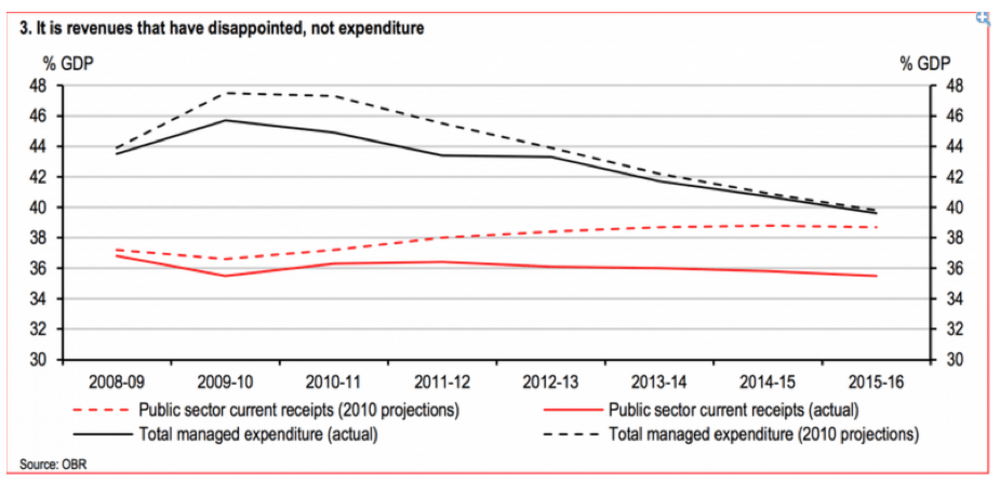

This chart from HSBC Economist Liz Martins shows why Mr Osborne failed to “slash the deficit.” He cut spending and public investment, and the outcome was that tax revenues fell, and the deficit rose. The dotted red line shows what Mr Osborne expected would happen to tax receipts if he cut government spending. The red line shows what actually happened.

The black line shows the steep decline in government expenditure as a percentage of GDP.

Which all goes to show: unlike a household, cutting government investment and spending when the private sector is weak, can increase, not eliminate the deficit.

[1] The deficit of 3.1% referred to by Business Insider is for the current budget, i.e. excluding investment borrowing. With investment borrowing, it amounts to around 4% of GDP

3 responses

No. It is true that certain government spending can help increase the economic output of the country… but most has the opposite effect. This is due to the fact that taxation is the necessary source of government spending, and the dead weight cost to the market caused by taxation (via decreased incentive) is almost always larger than the benefits gained from the government expenditure it is used on.

There is no evidence whatsoever to suggest that the dead weight cost by taxation is larger than the benefits gained through government expenditure. And rightly so it would be impossible to take everything into account. However its a more intuitive argument that the money spent by governments goes into areas of market failure – healthcare, education and upholding institutions. Which all economists agree are extremely important to economic growth and the proper functioning of the economy. I’d say losing these principles to reduce expenditure a little does much more harm than good.

Kitty Ussher on R4 yesterday said that Labour should support Osborne’s proposal and go further…