“The UK’s principled position is that social policy should primarily be a national responsibility, and it has used its influence as an EU member to reduce the impact of EU labour market regulation on the UK” HM Treasury analysis, para. 1.101 The long-term economic impact of EU membership and the alternatives

Summary

This article argues that the Treasury’s reports on the long-term and short-term impact of Brexit are misleading in the way their assessments – which are little more than guesstimates – are presented. They notably fail to make explicit the baseline for GDP against which the alternatives are assessed. The long-term report concentrates on trade and FDI as if these were the only key economic factors, ignoring the essential role of demand and overall investment. Having one of the world’s most deregulated labour markets, with least employment protection, is seen as a desirable economic policy goal.

But while we simply cannot sensibly quantify how things will work out 15 years from now, it is hard to see how a post-Brexit UK’s economic performance, including trade, would be any better if the same broad cluster of neoliberal policies is pursued by post-Brexit governments. On the contrary, it is likely that it would be somewhat worse. In the short term, the only way of preventing or limiting a recession due to Brexit uncertainty would be an aggressive use of fiscal and monetary policy, which is however politically unlikely.

The EU has delivered many gains for working people, but its economic policies – notably in relation to the eurozone – have failed. The existing Treaties prevent democratic economic alternatives to neoliberalism, and we need to work with partners across the EU to change them. For the UK to “walk away” now from the EU, with a government dedicated to a mix of ultra-free trade dogma, unregulated capital and right-wing nationalism, would change matters only for the worse.

Statistics and suspicion

Both the Leave and Remain camps suffer from deep public suspicion that they are dealing in propaganda rather than truth. The Leave camp have been tarnished by the false claim that, once EU membership ceases, the UK government would save some £350 million per week (£18 billion per year, or about 1% of GDP) which could be redirected in its entirety to other uses. The likely net “saving” is in fact about half this.

But there is almost as much distrust (not without cause) over the Treasury’s estimate of the likely “hit” to the economy that it claims – according to its own models – would flow from Brexit. What has caused particular concern is the Treasury’s claim to quantify the economic disadvantages it identifies – and the misuse by government “Remain” ministers of those statistics. A key problem is that the Treasury fails to set out the baseline assumption as to how GDP would develop if we remain in the EU. Instead, it set out statistics to make it look as though, for example, GDP in 14 years’ time would actually be 3.8% or 7.5% lower than now – which is not what the numbers mean.

The Treasury, to recall, has published two reports on Brexit. The first, published on 18th April, looked at the alleged long-term consequences from trade and FDI effects. The second, on the “immediate” economic impact, was published on 23rd May.

The Treasury’s long-term impact report

The Treasury’s model claims to calculate the outcomes of three possible future trade-relationship options in case of Brexit, and the report summarises them as follows:

But what do the numbers mean? The heading here does say, “difference from being in the EU”, but this is a very coy way of expressing what has been done, especially since the baseline scenario (Remain in EU) is not set out anywhere for straightforward comparison. For example, -£4,300 from what?

This is an egregious failing, since (a) it seems highly likely to mislead the ordinary reader, and (b) it is quite implausible that the Brexit “loss” would be of the same order against a baseline of average GDP rises of say 1% per year, as against 3% a year. Of course, the report’s failings in presentation have been compounded by the public misuse of these statistics by government ministers, in particular in implying that the “differences” in GDP per capita (which mean lower increases) were actual losses in household income.

We may assume that the Treasury “baseline” assumption is of average real GDP “growth”, over the next 15 years, is 2.1% or 2.2% per year. For comparison, the average annual change in real GDP over 43 years of the UK’s membership of the EEC/EU is 2.2%, while the increase in GDP per head of population is lower, at 1.8% per year.

But over recent years, which also cover the period of the great financial crisis, performance has been worse:

In the 21st century, the average annual change in GDP is 1.9%

In the 21st century, the average annual change in GDP per head is 1.25%

The absence of an explicit baseline “Remain” scenario (even expressed as a range)

The unbalanced concentration on trade and foreign direct investment (FDI) to the virtual exclusion of other dimensions that substantially affect the economy, and in particular

The paper says almost nothing about aggregate demand, which is key to the future. It assumes that “free trade”, foreign investment and supply-side issues are the only ones that are important, and that only by increasing ‘trade’ can you increase wellbeing.

Moreover, as the passage quoted at the head of this article shows, the Treasury report underlines the government’s commitment to reduce any social policy or employment protection provided at European level to an absolute minimum.

The role of trade and FDI

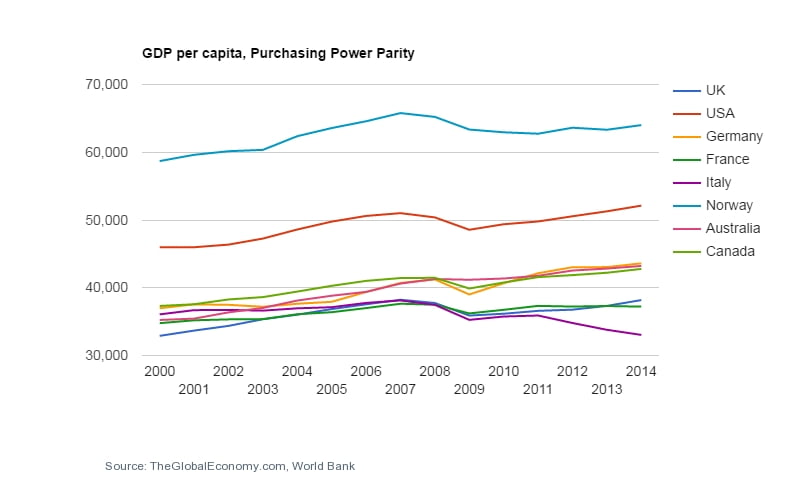

The Treasury’s central argument is that the EU single market and trade regime has been of particular advantage to the UK, which it would lose out on if it left. In fact, this is difficult to establish statistically, as it would requires an assessment of progress of countries inside and outside the EU, also allowing for other factors. Thus, for example, the development of UK GDP per head of population (in purchasing power parity) has run in close parallel with France (till 2012), and at similar rates to non-EU countries such as Australia, Canada or the US.

In terms of real GDP alone (ignoring population change) since the 1980s the UK has tended to increase at a faster average rate than other major EU states, but less than Australia or Canada in recent years. Overall, the EU as a whole has under-performed other advanced economies in recent years, largely due to the failings of the single currency.

Thus, it is actually difficult – when one looks at actual data rather than models – to quantify the GDP advantages of membership of the EU (which is not to say there are none).

The Treasury document argues

“In the long term, greater openness to trade and investment boosts the productive potential of the economy. Openness increases competition among firms, allows access to finance from abroad, improves the quality of production inputs, and creates incentives to innovate and adopt new technologies. The HM Treasury analysis estimates the impact on trade and FDI and what this means for productivity and GDP under EU membership and the alternatives. Higher productivity means better quality jobs which lead to higher real wages and household incomes.”

It is not my purpose to deny that much trade brings benefits to citizens and in the productive capacity of a country. Likewise with productive inward investment that is committed for the long-term. But once again, the modelled benefits are hard to quantify clearly when one examines the real-life GDP data. The “free trade” dogma assumes that increasing all kinds of trade is always and everywhere positive – which we increasingly understand is not the case.

In reality, different countries have achieved different balances in terms of trade and other economic drivers. Here is a snapshot (2014) of the widely differing position of exports as a percentage of GDP in a set of “advanced” economies (imports are broadly similar, allowing for trade deficits and surpluses). Now it is natural that the US – with its vast internal market – would have a much smaller share of GDP attributable to trade, but generally, there is little correlation between the trade density of each, and the actual economic outcomes (compare e.g. UK and Italy). There is a greater (but far from strong) correlation between size of population and trade density.

The next two charts show the development of UK exports from 1960 onwards, as a percentage of GDP. The first shows the UK compared to some other major economies, the second is the UK alone. It is evident from this that soon after the UK’s entry to the EEC/EU, exports started to play a more important role in the UK economy, rising from around 18-20% GDP earlier to 25-30% thereafter.

However, the average real annual GDP “growth rate” did not rise during the post-EEC entry period compared to the pre-entry period. While there is clearly some relationship between the development of trade and of GDP, there is a far from a close correlation over time.

The fluctuations bear some relation to economic activity, but for example we see a lower trade share in the late 1980s to early 1990s – a period which saw both the Lawson boom and recession. By contrast, exports as a % of GDP fell much less during the 2008-09 crisis but then rose sharply at a time that GDP did not.

Yet the Treasury report simply says this about the benefits of trade as a member of the EU:

“Membership of the EU has made it easier to trade both with the EU and the wider world. Trade as a share of national income has risen to over 60% in the past decade, compared to under 30% in the years before the UK joined the EU. The HM Treasury analysis, which is in line with academic research, shows that EU membership increases trade with EU members by around three quarters.” [1]

They do not argue here – but see below – that increased trade leads directly to stronger GDP. The issue leads us into complex issues of causation. The Treasury instead argues that there is a more general correlation of “openness” and economic success, since causation is elusive. If this is correct, at least in the way globalisation has unfolded to date, the point underlines further the problems of quantifying precise ranges of losses of GDP if the UK leaves the EU.

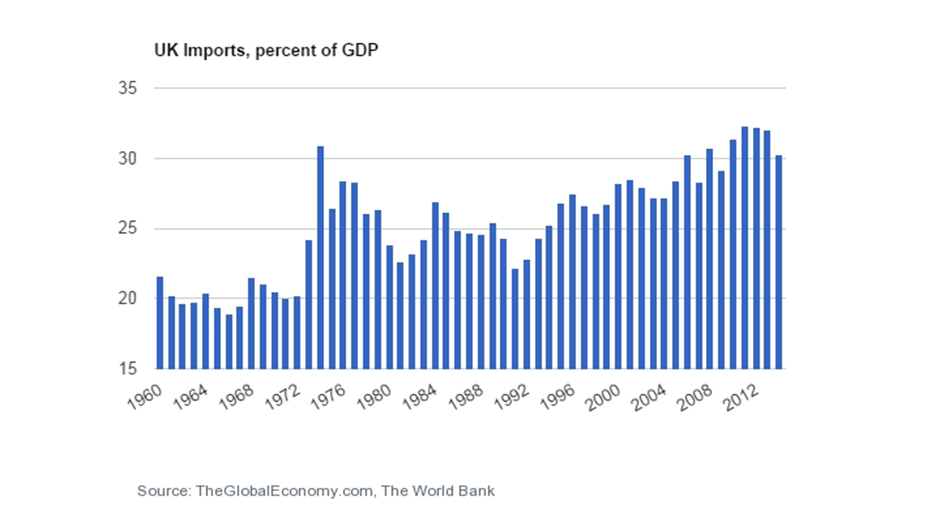

The issue for the UK is not just the level of trade but the balance of trade. If exports fell slightly but imports fell further, then (all else being equal) GDP would increase. Our trade deficit is currently around 2-3% of GDP. In the imports chart below, we see however that imports have exceeded 30% of GDP in 8 years, and recently by significant margins, while exports have only recently – and modestly – reached that level.

Foreign direct investment

The Treasury report says:

EU membership has also made the UK an attractive place to invest and one of the top global destinations for FDI. Almost three quarters of foreign investors cite access to the European market as a reason for their investment in the UK.

This may be factually true. But again, it does not help us draw conclusions about the quantitative impact of leaving the EU, since there is no clear way of calculating how far inward FDI actually tends to increase GDP, or how much would be lost if we were to leave the EU.

The next chart shows that for most of the period of our EU membership, annual FDI has been in the region of 2.5% of GDP per year – the two exceptions are the late 1990s, and the period just before the great financial crisis. Both these periods are in fact “boom” periods, followed by the dotcom crash first, and the GFC disaster in the second. There is no reason to believe that these boom-related FDI surges have long-term GDP benefits. Since 2008, we have returned to the earlier more modest percentages.

According to the Treasury report:

“The total stock of inward FDI to EU countries, which includes FDI from other EU countries, was $8.8 trillion in 2013, of which $1.6 trillion (18%) was invested in the UK. This made the UK the largest recipient of FDI in the EU, ahead of Germany and France (with inward FDI stocks of approximately $1 trillion each).”

A very recent OECD paper (“FDI in Figures”, April 2016) tells us that globally

“FDI increases by 25% in 2015, with corporate and financial restructuring playing a large role… OECD FDI inflows almost doubled in 2015 (to USD 1 063 billion) compared to 2014, reaching their highest level since the beginning of the financial crisis. However, they remain 19% below their peak level in 2007… The increase in the first half of the year was largely due to record levels of FDI inflows into the United States… due to some large cross-border deals.”

All this should make us suspicious of any causal link – globally or nationally – between surges in FDI and GDP. 2015, we may note, was a year in which global GDP advanced only very modestly (3.1%).

The scale of FDI into the UK, compared to other EU countries seen as economically “open”, is not matched by any evident ongoing superiority of economic performance.

The Treasury report also seeks to make a link with increased productivity (1.77):

“There is strong evidence that UK trade and investment has been higher as a result of this access to the Single Market. This has increased productivity in the UK. Higher productivity means better quality jobs, and higher real wages and household incomes.”

The problem with this statement is that productivity in the UK lags far behind most other high-income EU and OECD countries and in recent years has not been growing rapidly, over a time when FDI has been increasing and the stock is far greater than elsewhere except the USA. Either the increases in FDI have not had the claimed impact on productivity, or the rest of the economy is indeed in the direst condition.

Per hour worked, UK productivity is far worse than France’s, even though GDP has risen faster than France’s. France’s trade, we may note, is similar in scale to the UK’s, while her FDI is somewhat smaller.

Can we quantify the benefits of trade and FDI?

When it comes to assessing the GDP benefits of trade and FDI, the Treasury report is notably thin on evidence from actual data, and they fall back on academic modelling of results.

The clearest claims are these:

“Frankel and Rose (2000) estimate that a 1 percentage point increase in the trade to GDP ratio increases GDP per capita by 0.17% to 0.33%”.

Feyrer (2009) uses the relative cost of transporting goods via air following changes in transportation technology as a proxy for trade costs, estimating that a 1% increase in the growth rate of exports is associated with a 0.5% to 0.75% increase in the growth rate of GDP per capita.”

Taking the first, we may note that the increase in trade since joining the Common Market is some 20 percentage points, and we can assume that GDP per head has grown at roughly the same rate as GDP. So according to Frankel and Rose, GDP per head should be some 4-7% greater than if trade had not increased. But already by 1976, trade already formed around 56% of GDP compared with just over 60% today – which would mean that the increase in volume of trade since 1976 has had virtually no impact on GDP or GDP per head!

The second study (Feyrer) is more difficult to assess. What the author actually claims – working solely from air freight stats – is this:

“An increase in the volume of trade of 10 percent will raise per capita income by over 5 percent.”

Therefore, an increase in trade volume of 20% will raise per capita income by over 10%. Once again, this is extremely hard to reconcile with actual UK GDP per head data and trends over time, though he argues that Frankel and Rose’s conclusion is too high. Feyrer also raises the causation issue, positing that trade may be a proxy for a set of economic integration factors rather than a causal factor in its own right.

As a simple exercise, I have looked at the trade and GDP data for the UK, France, Germany, USA and Denmark, taking 1990 and 2014 as the two dates. I have calculated the percentage changes in trade and GDP (including GDP per head) and then looked at the ratios that flow. Since this depends on the specific years selected, I do not claim it has scientific force, but it does cover a 25 year period during which the EU single market has largely been operative. The curious result is that the UK is the economy in which trade increases appear to have had the lowest relative impact! [2]

Again, none of this is to argue that much trade and FDI is not of great value, but trade and FDI have to be situated in an overall context of strengths and weaknesses in an economy, and notably the state of demand and overall investment. There is no magic link between growth in trade and increase in GDP.

Demand in the economy

The report’s analysis is narrow in its focus. Above all, and true to its commitment to self-defeating austerity, the Treasury does not consider the issue of demand in the economy, nor other possible developments in the UK economy that could raise national income and develop wider economic activity.

Over a long period, the key weakness of the UK economy has been the low level of investment. Whether in or out of the EU, increasing capital investment as a proportion of the economy is necessary and the most reliable way of maintaining strong economic activity.

The chart below shows just how far we lag behind all comparator countries. The issue is the overall level of useful investment, public and private, not just (or mainly) foreign investment. The Treasury report at one point implicitly accepts that it is overall investment that is the key to productivity, but fails to draw a wider conclusion:

“Access to the Single Market affects the incentives of businesses to invest in the UK, both for domestic firms and foreign firms. This matters because investment in the economy is a key determinant of economic output and productivity growth.” (My emphasis).

It is of course true that specifically foreign investment can have some advantages, as the Treasury report says:

“Evidence suggests that FDI can increase local productivity by influencing the composition of the economy and through positive knowledge spillover to domestically-owned firms.”

But this does not affect the fact that domestic investment is even more important. If FDI per year is 2.5% of GDP, and overall investment is say 18%, that leaves 15.5% that is not FDI!

The failure of the Treasury report to focus on demand reflects its ideological bias towards austerity, but it is still a remarkable lacuna. After all, the same bodies (IMF, OECD for example) that have voiced support for the UK Remain case have been pressing the case for more active fiscal policy, notably investment.

As Narayana Kocherlakota, till recently President of the Federal Reserve Bank of Minneapolis, put it in a Bloomberg article on 21st April:

“A disease – persistently low demand for goods and services – has afflicted the world economy… It’s puzzling and deeply disturbing that fiscal policy makers aren’t doing what they can to cure the global economy’s disease.”

A post-Brexit government could in theory change course and undertake a large-scale public investment programme (though given its likely political direction, this seems a most unlikely outcome). The Treasury does not even consider this possibility.

The Treasury report – the short-term impact

On 23rd May, the Treasury released its second report, on the “immediate” impact of a Brexit vote. The report summarises the position:

“A vote to leave would cause an immediate and profound economic shock creating instability and uncertainty which would be compounded by the complex and interdependent negotiations that would follow. The central conclusion of the analysis is that the effect of this profound shock would be to push the UK into recession and lead to a sharp rise in unemployment.”

They claim to quantify two possibilities – a “shock” scenario, and a “severe shock” one. These are summarised in a similar chart to that included in the long-term report. This time, the heading at least refers to the “% difference” from base level, though again without being explicit as to that level:

The OBR March 2016 forecast is for GDP to rise 2% in 2016, 2.2% in 2017 and 2.1% in 2018. Here is the Treasury’s assumption of how such “shocks” might follow through:

The OBR assumption for CPI inflation in 2017 is 1.7% – add on 2.3 % points and we get to 4%, which would be a huge sudden increase indeed, and this becomes inflation of 4.4% under the “severe” scenario. The projected falls in the exchange rate and in house prices would in themselves be capable of being advantages, but the likely increase in unemployment flowing from any recession is a major concern – even if the Treasury’s numbers here are again open to question, and little more than model-generated guesstimates.

Conclusions

Back on 10th May, weeks before seeing the Treasury’s short-term impact, I wrote this, linking the long-term report with my thoughts on the immediate impact:

“In the end, I share just a little of the Treasury’s perspective, though I do not share their economic philosophy nor propagandistic approach. It is hard to see how and why Brexit – assuming the same free-trade philosophy of the successor government as of the present government – should lead to any better outcome in terms of trade, at least for quite a long time, and some good reason to believe that the situation would be worse. It is not as if the UK is heavily regulated in terms of labour protection. On the contrary, the OECD tells us that we are… in the bottom 3 most deregulated countries in the world as regards employment protection.

Moreover, a “Leave” vote would assuredly lead to a period of uncertainty in terms of FDI and of domestic private investment. The negotiation inside the EU will last for at least 2 years, to be followed by any residual uncertainty about what is to happen. This would need to be countered by a large-scale public investment programme – but it is hard to see that the new right-wing Brexit-negotiating government would have this on its agenda. It is likely to be even more economically orthodox and deficit conscious than the Cameron-Osborne government…

So if we have a fall in private investment which is not matched and indeed surpassed by an increase in public investment, a tough recession seems likely. A government committed to a more “autarkic” policy might be able to deal with the situation, but that is not what we will have. I do not think that the current slowdown in the UK economy is caused by the Referendum campaign’s shadow, but it does seem that a decision to Leave would coincide with an already difficult situation.”

This remains my view. Moreover, the slowdown in the UK economy over the last year would provide a particularly difficult moment for a new “Leave” government, and make a Brexit recession more likely. All this might not matter so much if it were not for the trade and current account deficits. We have to consider that the pound would rapidly and significantly fall in value, and that the trade gap could become even larger if this sucks in imports faster than exports grow. And the willingness of foreign investors to fund the current account deficit without a large premium has to be considered.

In the short term, the only way to combat recession would be an aggressive use of combined fiscal and monetary policy, including a sustained major public investment programme. But do we really envisage a right-wing government driven by the leading Brexiteers to do the biggest policy U-turn in political memory, overturning austerity and deficit fetishism?

Looking to the long-term, we simply cannot foresee how things will work out 15 years from now, though as indicated, it is indeed hard to see why economic (including trade) performance outside the EU would be any better if the same broad cluster of deregulating neoliberal policies is pursued by post-Brexit governments.

The European Union is at a dangerous point – some of it (but far from all) self-inflicted by its economic errors. If the UK pulls out at this juncture, the winners in the UK will be the even-more-ultra-free-trade pro-deregulation wing of the Conservative Party – allied de facto to the right-wing nationalism of UKIP. And if the UK votes to leave at this juncture, it will invigorate all the ultra-nationalist forces across the continent, and could even start a process leading to the disintegration of the Union led by right-wing nationalist forces. If this happens, we cannot guarantee that the EU’s biggest achievement – long-standing peace on most of our continent – will endure.

The EU has delivered big gains for working people in the past. Women’s rights, workers’ rights, environmental and consumer protection, climate change, international development, help for poorer EU regions – a big yes in many respects. These remain relevant and significant. But seriously, the policies of the Eurozone have not delivered prosperity or social justice for working people. It is unacceptable to have unemployment above 10% for year after year. The Eurozone economic policies and means of enforcement have been a disgrace and greatly damaged economic activity.

We have to get the balance right, if the EU is to remain viable for the future. And that means the long hard slog of forging the solidarity and pressure to change the damaging economic policy straitjacket of the Treaties, which impose an odd mix of neo- and ordo-liberal dogma, and block democratic economic choices. But for Britain to walk away now into its own quagmire of deregulated free trade dogma and right-wing nationalism will change matters only for the worse.

But – Labour Party members please note – the “Remain” camp within the present Conservative government are absolutely committed to preventing any positive gains from the EU on social policy and workers’ rights. Their vision of Europe is of deregulated globalisation, with finance capital unleashed.

So yes, I will vote Remain in the referendum in June, but not based on the arguments or exaggerated presentations of the Conservative “Remain”.

Jeremy Smith is Co-director, Policy Research in Macroeconomics (PRIME), and formerly Secretary General to the Council of European Municipalities and Regions

Footnotes

[1] The Treasury report uses a different basis of showing trade/GDP from those we have used from the World Bank. We show exports and imports as a percentage of GDP year by year, while the Treasury state “the trade-to-GDP ratio is the sum of real exports and imports divided by real GDP in 2012 reference prices. The latter methodology shows a relatively seamless upward trend from the 1970s until the 2008/09 crisis, when it flattens.

[2] For example, the ratio ‘% change in GDP per capita : % change in exports in $’ is 5.8 for the UK, but 7.6 for France and the US, and 8.9 for Germany. The UK had the biggest percentage increase in GDP per head, but the second smallest percentage increase in exports.