Image via https://ebooks.adelaide.edu.au/c/coleridge/samuel_taylor/rime/

Today we had the first estimates for 2nd Quarter GDP for both the Eurozone (from Eurostat) and the United States (from the BEA). Both sets of data give cause for concern that the world economy – and in particular the so-called “advanced economies” are stuck somewhere in the doldrums between sluggishness and stagnation.

According to Eurostat, Q2 GDP in the Eurozone rose by just 0.3%, a little down on the Q1 0.4%. France managed just zero (after +0.7% Q1), while Germany is likely to have been lacklustre. Looking at the year-on-year position, GDP was up by 1.6% compared to the same quarter in 2015 – a really miserly performance given where one should be in the cycle, but heavily explained by the fact that the unemployment rate for June – also announced today – is still a vast 10.1%. It has been over 10% – save for one solitary month – since autumn 2009. While Spain’s unemployment fell by 57,000 on the month (but remains over 4.5 million), France’s sadly rose again by 20,000, and Italy’s by 27,000.

Worrying US data

More concerning, and perhaps more surprising, were the Q2 results from the United States. Here to the quarter-on-quarter increase in “real” GDP was just 0.3%, annualised (in the US manner of presentation) as 1.2%. This followed a revised (down) annualised Q1 of an exiguous 0.8%, following 0.9% for Q4 2015.

Comparing Q2 2016 with Q2 2015, we see that the actual annual increase was also just 1.2%, down on the Q1 increase of 1.6%. The Q2 figures are very disappointing, given that the US employment and unemployment figures have seemed to be relatively strong recently, with the official US unemployment well below 5%.

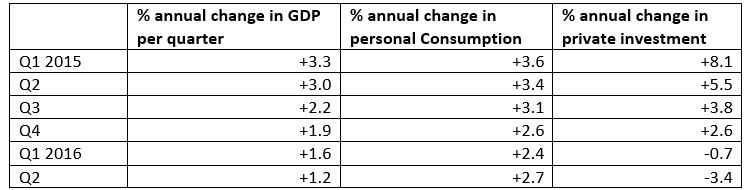

In fact, we can see that the US economy has been decelerating (taking the annual rate of change) quarter by quarter for over a year.

While personal consumption has held relatively firm in Q2 in volume terms, after slowing in previous quarters, private investment has continued on a sharp downward slope. Here is a Table showing the annual percentage rate of increase in GDP per quarter from Q1 2015 to Q2 2016, together with the figures for private consumption and investment: