When I last twice travelled directly to Guangzhou, by China Southern Airline out of Heathrow, the flight was nearly full. But not – by visual impression at least – full of thrusting British entrepreneurs keen to visit the most vibrant economic region of China, thanks to this direct link from Britain’s hub airport. More like ordinary Chinese workers and some visitors. No – increasing trade is a more complex issue by far.

Which is one of many reasons why I was truly jaundiced reading Heathrow Airport’s advertisement yesterday, which compiled a list of highly dubious claims as to the benefits to all of us in the UK of a 3rd runway at Heathrow. I have no doubt that a 3rd runway there would be of benefit to the shareholders of Heathrow Airport, and might conceivably be nicer for passengers, but the specifically economic case for choosing Heathrow over say Gatwick – or indeed Boris Island – is still as thin as ever.

Yet we are being bombarded with phony or super-fragile statistics trying to bludgeon us into thinking that the UK will collapse economically overnight if those 3,500 metres of tarmac are not built tomorrow morning on Heathrow’s green and pleasant land.

Two years ago to the day we produced a short paper “Why the economic case for a 3rd runway at Heathrow still won’t fly”, and 2 years on, it still doesn’t.

Heathrow’s dodgy claims

Among the dodgy economic claims by Heathrow Airport for the 3rd runway:

• It will bring economic benefits of £100bn • It will bring 120,000 new jobs • Every month the problem goes unresolved is costing the British economy £1.25bn through lost trade

The evidence for each of these is very thin and hypothetical – like money, created out of thin air. The link between trade and airport capacity is at best indirect, and certainly opaque. At a macroeconomic level, the impact is simply invisible.

Let us look at the overall national GDP figures in recent years for the main European countries with major hubs – the UK (Heathrow), France (Charles de Gaulle), Germany (Frankfurt), Netherlands (Schiphol), Madrid…

From Eurostat, here in the first column is the average % change per country in GDP between 2003 and 2013, the period when Heathrow’s competitors have been swiftly expanding their hub capacity while Heathrow has been, we are told, capacity constrained. And in the second column, the average % change in GDP from 2008 to 2013

2003-13 2008-13

UK 1.4 0.03

Netherlands 0.9 -0.25

France 1.0 0.11

Germany 1.2 0.73

Spain 1.1 -0.97

See a clear pattern? See how a rapid rise in hub capacity grows your economy faster? Er, no. There is simply no pattern to be discerned. Economies depend on many factors, and hub capacity is one of the least significant, at least once you reach a decent threshhold of scale. Over the whole 11 year period, the UK has “grown” on average faster than its “competitors”. Since the great crash of 2008, Germany has grown on average faster, and France a teensy weensy bit faster, than the UK, while the Netherlands – with rapid growth in capacity and destinations at Schiphol – has slumped and Spain has spiralled downwards. (If we look further afield at at JFK New York, its passenger numbers are tiny in comparison with Heathrow. Yet New York’s economy still seems to be standing.)

You may have noticed that the hub-constrained UK seems to be increasing GDP more than the Eurozone-constrained but hub-growing rivals in 2014, with the UK almost certain to leap ahead of France, for example, if one averages GDP changes from 2008 to 2014.

Heathrow Airport’s favoured consultant economists, Frontier Economics, contend that with a full unconstrained hub in Heathrow, UK GDP would grow by around 1% per year – hence the silly statistic above that claims we are losing £1.25 billion per month because the “problem” is not “resolved”. But they do not back this up with any firm evidence. It is pure – and implausible – hypothesis.

The other statistic – economic benefits of £100 billion (over what period, the ad does not say) is around 6% of UK GDP – a big change if ever achieved over a single year (the chance of which is zero). But since there is no evidence of overall economic national economic gain from new hubs, please maintain due scepticism.

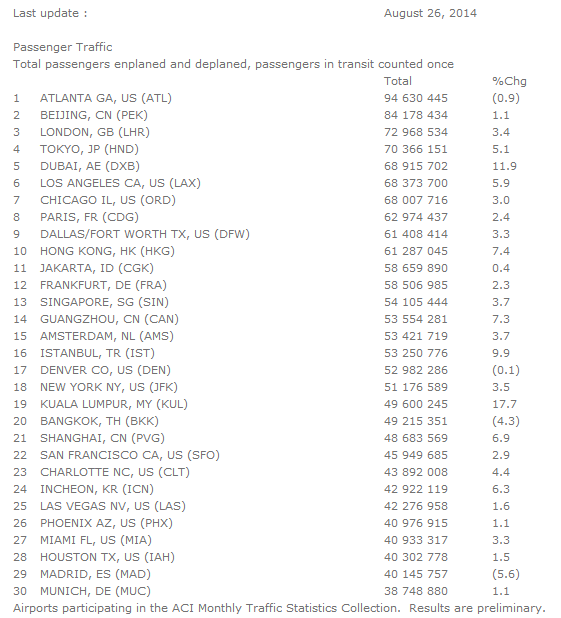

Heathrow still Europe’s No.1 passenger hub

The truth is that Heathrow remains Europe’s largest hub airport, in terms of passenger numbers passing through, and its “competitors” are only slowly catching up – if at all. Combine with Gatwick, the London capacity and throughput is hugely greater than any other European capital. Here are the latest figures from the Airports Council International for the12 months to end of May 2014 :

airport passenger numbers 2013-4

For all the scare tactics, Heathrow is still way ahead of other EU hubs, with 10 million more passengers than Charles de Gaulle, 14 million more than Frankfurt, and 19 million more than Schiphol. And what is not explained is why it would matter if another European country’s hub caught up with London, since “big hub” does not equal “better economy”.

CBI joins in the propaganda

Alas, the CBI have also leapt in (in what looks like an engineered lobbying exercise) using the same flawed logic as Heathrow Airport:

“With the UK’s hub capacity at Heathrow already full, the UK is falling behind on direct flights to emerging markets. … [T]he UK’s EU competitors with their own unconstrained capacity are creating connections to new destinations within the BRICS such as Xiamen in China and Recife in Brazil, as well as links to the major markets of the future, like Peru, Indonesia, Taipei and Chile.

Katja Hall, CBI Deputy Director-General, said:

“The Chancellor has set businesses ambitious targets for increasing the UK’s exports, and there is simply no way of achieving these goals without upping our game in emerging markets. Our analysis last year demonstrated that connectivity is the lifeblood of trade, but it also highlighted that the UK is already falling behind, so every day we delay making a decision, makes matters worse.”

Again the meme, “every day we delay makes matters worse..” as if repetition makes it true.

What is never explained by the propagandists is that each country’s hub serves a set of destinations that has in part a historic logic. Thus Paris serves the French ex-colonies, Heathrow the British ex-colonies and the Anglosphere, while Frankfurt has more flights into Russia. Of course it is a good idea to have more flights to China and fast-growing economies, and Heathrow is indeed weak in China direct flights. But it is stronger than the other hubs in its India links. Each hub has relative strengths and weaknesses, and they can’t all fly everywhere.

Cooperation not competition for the EU hubs

What is wrong, indeed dangerous, is the whole notion of a competitive race between EU hubs. The Heathrow ad says

“While Britain wrings its hands over the site of a new runway, our competitors in France, Germany and the Netherlands are rubbing theirs. They have the hub capacity. They have the will to grow it. And they have the wholehearted support to take what could be Britain’s.”

Twaddle. It is physically impossible for all countries to have a spoke and hub system that links to every big city in every country. It is even more undesirable to do so, in terms of the global environment and climate change. At the margins, there will be some competition for routes. But in essence, the EU hubs need to cooperate.

From the perspective of a British resident wanting to travel to another continent (say, Asia), unless you live in a big city and are able to travel to another big city directly, you are likely to need to travel through a hub. But whether it is in the UK or elsewhere is of frankly little importance. So whether you change at Heathrow, Schiphol or Singapore is neither here nor there – it depends on timing, convenience and quality of experience. And this is so whether you are a tourist or businessperson.

You can succeed even without a hub!

Many countries are successful economically without having a major hub airport. Take Sweden and Austria for example. As Europeans, we need to use cooperation and common sense when it comes to transport infrastructure. Not simply pretend that we can forever scavenge for finite, minuscule economic benefits that we try to steal from each other.

It is for government and the aviation industry, at UK and EU levels, to agree a strategy for which destinations across the world are deemed strategically important – whether for trade or other purposes. The use of our airports should reflect this national and European interest, not just “market forces”.

The current debate assumes exponential growth both of our economies and of our travel into the indefinite future. This will not happen as there are natural limits imposed by the earth’s resources. Airports are important and need to be pleasant and reachable places for business and leisure. But they are not the main drivers of economic success nor of national well-being. Resist the self-interested lobbyists!

Appendix

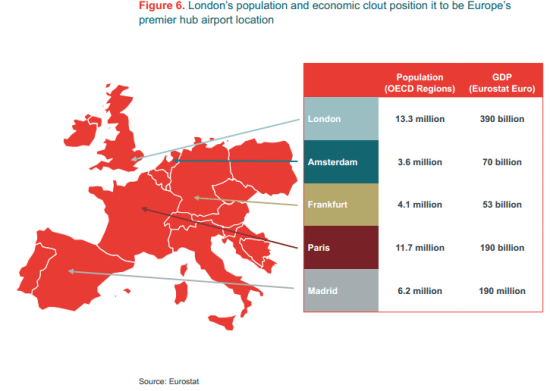

Among the many dubious economics-related points made by Frontier Economics, the following chart has puzzled me in particular. It comes from their September 2011 “Connecting for growth: the role of Britain’s hub airport in economic recovery” report which was “prepared for Heathrow”.

London and Paris economies

This gives London’s population as 13.3 million, taken from OECD figures, I presume for metropolitan regions. This includes Greater London (Boris’s bailiwick) plus significant parts of south-east England. Its regional GDP is given as Euro 390 billion. Paris, by comparison, has a population of 11.7 million, which presumably is that of the Ile-de-France region (though the source year is not given), and the regional GDP is a mere Euro 190 billion, or just half that of London (but with 5/6ths of the population). The source is said to be Eurostat for the whole set of information.

On 21st March 2013 Eurostat published a short release on “Regional GDP per capita in the EU in 2010″, in which it gives the Ile-de-France GDP as Euro 588 billion, with an average GDP per head of Euro 49,800. London’s GDP is also given, as Euro 362 billion (of which inner London including the City is Euro 250 billion) but this is for the GLA area alone, which has a population of around 8 million not 13 million; the GDP per head is a little below Paris’s at Euro 46,300. If you add the entire south-east (which goes well beyond London’s natural economic region) this would add a further Euro 244 billion of GDP, or a total of London and south-east of Euro 606 billion, a little more than Ile-de-France’s but with a larger population.

So if my reading of Eurostat’s figures on regional GDP are right, it must mean that Frontier Economics’ figures in this important chart are completely wrong. Even though they provide no year for their figures, the difference is so extraordinary that it could not be accounted for by annual changes. What is even more suspicious is that Madrid’s GDP is also given as Euro 190 million (surely this is a misprint for billion?), though it has only just over half of Paris’s population.

Yet their chart is entitled “London’s population and economic clout position it to be Europe’s premier hub airport location” – an honour which, on my understanding of the true facts, should be shared with Paris and the Ile-de-France.

If as appears to me Frontier Economics have got their facts wrong on this chart, and given that there are clear accessible sources for the information as they present it, then it further enhances my doubts about their economic statistics and estimates in general – on which Heathrow Airport rely in their propaganda. If (despite my doubts) Frontier can demonstrate with sources that they are right on the numbers in this chart, I will of course acknowledge this fully and prominently.

2 responses

Heathrow air traffic movements have grown 2.6% in the period from 2003 to 2012 and is capacity limited to 480,000 pa. In the same time UK GDP has grown by 9.5%.

Absolutely right – no need for a third runway at Gatwick either. The follow-on question is how aviation remains such a large, untamed lobby – lightly taxed, heavily pollutant, very good at up-grading MPs on their flights, I understand (not a declarable benefit because no money changes hands)