It’s Europe Day, and I for one am pleased that at last, Prime Minister David Cameron has today started to make a wider political case for remaining in the European Union. To be frank, the EU has big disadvantages, most notably in the economic sphere, with its Treaty-embedded mix of ordoliberal (Germany) and neoliberal (UK and several others) policies that are causing so much damage. And it is hopeless always to posit the case for “remain” on the basis of the assumed natural superiority of the British and their institutions, as our establishment so often do.

But I do agree with Cameron on this:

“How could it possibly be in our interests to risk the clock being turned back to an age of competing nationalisms in Europe? And for Britain, of all countries, to be responsible for triggering such a collapse would be an act of supreme irresponsibility, entirely out of character for us as a nation.”

The European Union is at a dangerous point – some of it (but far from all) self-inflicted by its economic errors, and yet if the UK pulls out at this juncture, the winners in the UK will be the even-more-ultra-free-trade pro-deregulation wing of the Conservative Party who will have gained the upper hand – allied de facto to the right-wing nationalism of UKIP. A win for “leave” will empower UKIP further. And if the UK votes to leave at this juncture, it will invigorate all the ultra-nationalist forces across the continent.

Nor am I persuaded by the over-simplistic “Remain” argument of Labour MPs like Tristram Hunt in today’s Financial Times, who says

“No more fudging: it is in or out. On grounds of prosperity, social justice and European solidarity, Mr Corbyn’s case should be for a resounding Remain.”

But this will not wash either in that crude form. The EU has delivered big gains for working people in the past. Women’s rights, workers’ rights, environmental and consumer protection, climate change, international development, help for poorer EU regions – a big yes in many respects. These remain relevant and significant. But seriously, the policies of the Eurozone have not delivered prosperity or social justice for working people. It is a large number working class people in particular who tend to vote “no” in referenda, or vote for anti-establishment parties of left or right.

There are millions of Europeans who oppose the ultra-free-trade dogma that leads to TTIP and the empowerment of international corporations at the expense of people and their governments. It is unacceptable to have unemployment above 10% for year after year. The Eurozone economic policies and means of enforcement have been a disgrace and greatly damaged economic activity.

We have to get the balance right, if the EU is to remain viable for the future. And that means the long hard slog of European solidarity in a different sense from Mr Hunt’s – building the solidarity to change the damaging economic policy straitjacket of the Treaties. Britain walking away now into its own deregulated free trade wilderness will do nothing, change matters only for the worse.

So yes, I will vote “Remain” in the referendum in June. But that said, I think the Treasury’s recent paper on “the long-term economic impact of EU membership and the alternatives” – like most of the debate to date on economic issues – is narrow, based on a flawed or one-sided analysis, and is unconvincing in its impact estimations.

The Treasury model

As has been well-publicised, the Treasury argue that the UK will be better off economically staying in the EU than leaving, and then purport to estimate how much worse off we would be under three different options – mainly related to cross-border trade – as percentages of GDP, then translated into loss of GDP per household. Here is their table showing the range of quantified “losses”:

It is based on a complex model – set out in a complex equation – that claims to lead to the above specific ranges of outcome. It does not base itself directly on actual economic data from the EU, IMF or other international organisations.

The broad argument – that given no serious change in the economic philosophy and policies of a post-Brexit government, it is hard to see how leaving the EU will assist the UK in terms of trade performance, is one that I would tend to share. But the quantification set out above is based on so much hypothesis and assumption over the next 15 years as to be little more than one machine’s guesstimate.

The EU single market – a history of exaggerated claims

Now there is a long history of forecasting benefits from the EU’s trade and single market measures, with exaggerated estimations. Back in 1988, we had the Cecchini Report which sought to estimate the benefits from the Single Market measures that were due to take effect in and from 1992. Here’s what that report forecast:

The total potential economic gain to the Community as a whole is estimated to be in the region of ECU 200 billion or more expressed in 1988 prices. This would add about 5% to the Community’s gross domestic product…

The study further shows that the predicted effects of EC market Integration through removal of customs barriers, opening up public procurement, Iiberalisation of financial services, and other supply-side effects will in the medium-term

in addition to boosting output, employment and Iiving standards simultaneously cool the economy, deflating consumer prices by an average of 6%;

relax budgetary and external constraints, improving the balance of public finances by an average equivalent to 2.2% of GOP and boosting the EC’s external position by around 1% of GDP.

After about 5 to 6 years, a cumulative Impact of +4½% In terms of GOP and -6% In terms of the price level could be expected. The positive Impact on employment could in the medium-term amount to about 2 millions Jobs, even after absorbing the significant productivity and restructuring effects, attributable to the Integration of the market.

If a specific macroeconomic policy that recognized the potential for faster growth Is pursued; as would be reasonable to expect also in view of the lessening of inflation, balance of payment and budget deficit constraints, the gains could mount to 7% in terms of GDP and a 5 million increase In employment.

That was the prophecy. Fast forward to a review by Deutsche Bank in 2013 “The Single European Market 20 years on” which summarised the actual estimated outcomes, from a number of research papers. The reality, in DB’s view, was extremely modest, for example:

For the European Commission, Ilzkovitz et al. (2007) found that the Single Market generated additional income of 2.2% between 1992 and 2006. Stripping out enlargement to the East in 2004 the effect amounted to nearly 2%. The number of jobs in the EU is said to have risen by around 1.35%. Most of the impact was static in nature, however, while the dynamic effects due to increased investment activity and productivity gains have been somewhat disappointing to date. A more recent report, which also covers the latest episode of the crisis, makes nearly identical findings, namely additional GDP of 2.13% and a 1.3% increase in jobs. [My emphasis]

Even these “findings” seem on the high side compared to the Eurozone reality we have actually seen, notably since 2008 – even though the Euro (economic and monetary union) was itself supposed to be economically positive, additionally to the EU-wide single market. And eurozone unemployment has been above 10% for years…

But this history of exaggeration in relation to the potential of the Single Market did not end in 1988. In 2014, the European Parliament’s Research Service published a report, “The cost of non-Europe in the Single Market”, or “Cecchini Revisited”, whose Abstract states:

“This Cost of Non-Europe report seeks to quantify the costs arising from the lack of full achievement of the Single Market and analyses the benefits foregone for citizens, businesses and Member States. The report considers the economic cost of market fragmentation and of the gaps and shortcomings in five areas: the free movement of goods, the free movement of services, public procurement, the digital economy, and the body of consumer law known as the consumer acquis.

The report estimates that completing the Single Market in these fields would bring potential economic gains in a range between 651 billion and 1.1 trillion euro per year, equivalent to between 5 per cent to 8.6 per cent of EU GDP.”

Unlike Deutsche Bank, this report gives a more glowing estimate of the 1992 reforms:

“In its twenty years of existence, the European Single Market consisted is estimated to have raised GDP by 5%. When dynamic effects are factored in the measurable effect can be seen to rise significantly.”

Given the disaster that has befallen the Eurozone, it is extraordinary to claim such a high level in 2013. This constant GDP chart for “old” EU countries from 1980 to 2014 certainly do not seem to show much obvious development post-1992, save perhaps for Germany and the UK:

And if you take out the Big 4 (Germany, France, Italy, UK), it’s still hard to see any specific impact for the smaller economies, especially once the post financial crisis period is taken into account:

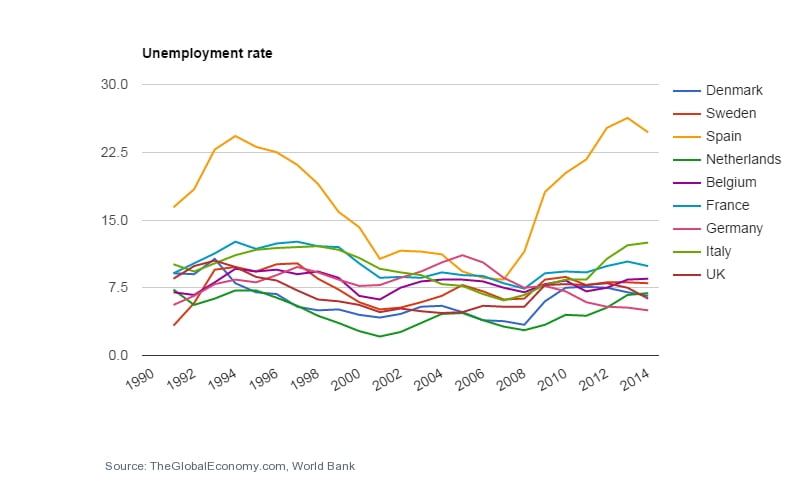

As regards unemployment (which I take as a proxy for growth in employment), I defy anyone to make any causal connections with the single market – four out of nine countries had a lower unemployment rate in 2014 than 1991, but 5 had a higher one:

Leaving Spain’s wild gyrations out of the picture, but adding the USA for comparison, we see how unemployment (and thus employment) has changed according to the cycle and Eurozone crisis – but nothing that remotely resembles a continuing improvement:

Concerns over the Treasury report

My main concerns with the Treasury paper are these:

(a) The Treasury give us no explicit baseline scenario (even expressed as a range) for the UK’s national income (GDP) assuming we remain in the EU. This is surely an essential step in the evaluation of other options. Yet they feel able to give quite precise quantifications of the alternatives, albeit expressed as a range, to be assessed against the “remain” scenario. If over 15 years there were seen to be no increase in GDP under the baseline scenario, then the alternatives would indeed be catastrophic. If baseline scenario “growth” was a huge 5% per annum, then the loss in 15 years’ time of (say) 4% of GDP against that would be far less significant, when weighed against other non-economic factors.

(b) The paper concentrates overwhelmingly on the issues of Trade and Foreign Direct Investment, as if they are the only important aspects of economic activity and well-being. I would argue that the evidence from actual real world results does not bear out the assumption that these are such critical factors as is assumed in determining the development of national income.

(c) The paper says almost nothing about aggregate demand. It assumes that “free trade” and supply side issues are the only ones that are important, and that only by increasing ‘trade’, can you increase wellbeing. In fact, it is aggregate demand – domestic as well as international – that is central to economic development and national prosperity, and trade mainly follows demand rather than causing it. Thus a proper analysis of the UK’s prospects inside or outside the EU needs to take many more factors into account, if it is to have any evidential or persuasive value. Especially the role of generating adequate demand. As Narayana Kocherlakota, till recently President of the Federal Reserve Bank of Minneapolis, put it in a Bloomberg article on 21st April:

“A disease – persistently low demand for goods and services – has afflicted the world economy… It’s puzzling and deeply disturbing that fiscal policy makers aren’t doing what they can to cure the global economy’s disease.”

What is the likely baseline for GDP if we remain in the EU?

So first question – what is the likely path of the UK economy if we stay in the EU or decide to leave? Surely the first thing to do here is to look at what has actually happened to date to GDP over time – yet for all its detail on other matters, the Treasury paper gives no place to actual experience. To deal with this, we need to look at both the development of GDP itself, but also – as a proxy for national prosperity – at GDP per head of population.

First, UK GDP since the late 1940s. ONS provide the following chart for the annual percentage rate of change of “real” GDP (i.e. after allowing for inflation).

We see that until 1974, in the so-called ‘Keynesian’ period there were no recessions, and while annual increases went up and down, the general rate was generally high. The next 20 years, which coincide with the process of financial liberalisation, were more turbulent and led to three sharp recessions, followed by the apparent calm of the mid-90s with “growth” of at least 2.5% per year till the global financial crisis struck in 2008 – the deepest recession in the post-war period followed by slow, modest recovery. It is once again hard to extrapolate any particular factors that can be strongly correlated with the benefits of the single market or the EU’s trading frameworks.

Turning to GDP per head of population, the next chart shows that for much of the post-war period, there was little difference in the evolution of GDP, and that of GDP per head of population. That is, GDP rose each year in line with the growth in the population.

However, from the mid-1990s that changed, with GDP per head rising to a lesser extent, and since 2004 the gap has widened even further, since the population (both from inward migration and domestic birth rate) has increased more rapidly while – since the crisis – austerity and low investment have held back stronger economic activity.

I have calculated the annual average changes in GDP for the whole 67 years since the ONS dataset begins in 1949, since if we are looking ahead 15 years or more, we need to look at the likely rate of evolution as informed by actual data and experience. The answer for this long-run period is 2.6% per year.

I have then broken this down, taking the period before the UK joined the EU (or EEC as it was) in 1973, and for comparison the same number of years after. The earlier ‘Keynesian’ 24 year period saw the highest average rate of GDP increase, 3.4%, while the first 24 years of EU membership (to 1996) achieved 2.3% on average. The final period, to 2015, saw the lowest annual average of all, 2.1%. Taking the whole 43 years of EU membership, the annual average is 2.2%.

• In the 67 years 1949 to 2015, the average annual change in GDP was 2.6% • In the 24 years 1949 to 1972, the average annual change in GDP was 3.4% • In the 24 years 1973 to 1996, the average annual change in GDP was 2.3% • In the 19 years 1997 to 2015, the average annual change in GDP was 2.1% • In the 43 years 1973 to 2015, the average annual change in GDP was 2.2% • In the 10 years 2006 to 2015, the average annual change in GDP was 1.3%

I have then looked at the figures for GDP per head over a slightly different period, as the ONS statistics start a bit later, in 1956. Over the whole 60 years, GDP per head has risen an average of 2.1% per year, but in the 43 year period of our EU membership, the average is 1.8%. This is not, to be honest, a very strong achievement, and the figures since 1990 are worse – a mere 1.5% per year average. Last and least of all, over the last 10 years (which include and are skewed by the financial crisis), the average annual rate of increase in GDP per head is just 0.5%.)

• In the 60 years 1956 to 2015, the average annual change in GDP per head was 2.1% • In the 17 years 1956 to 1972, the average annual change in GDP per head was 2.7% • In the 17 years 1973 to 1989, the average annual change in GDP per head was 2.4% • In the 26 years 1990 to 2015, the average annual change in GDP per head was 1.5% • In the 43 years 1973 to 2015, the average annual change in GDP per head was 1.8% • In the 10 years 2006 to 2015, the average annual change in GDP per head was 0.5%

As will be seen from the above, there is a tendency for the average to decline as we get nearer to the present. In case you think it is unfair to look just at the last 10 years, given the depth of the 2008/09 crisis, I have also taken the 21st century to date:

• In the 21st century, the average annual change in GDP is 1.9% • In the 21st century, the average annual change in GDP per head is 1.25%

To recap, we see that the average annual increase in GDP, over 43 years of the UK’s membership of the EEC/EU, is 2.2%, while the increase per head of population is lower, at 1.8% per year.

Looking to the future, then, if the UK remains in the EU we would surely be unjustified – if the policy framework is unchanged – to assume a long-term average GDP rate higher than +2.2% per year. It may indeed be more realistic to take a lower figure (the OBR have lowered their estimate to 2.1% as the basis for 2018-20). This would give, for the future, an average increase in GDP per head of around 1.5% – which is also the average since 1990.

This indeed would mean that that annual “growth” under any Brexit option would (if the Tresury model were reliable) be reduced to sustained historic lows. but it seems hard to see that the level of reduction would be the same as a percentage of GDP, however big or small the “Remain” assumption on GDP is. It is most odd that the Treasury does not make an attempt to set out the baseline or the likely path of reduction, given how concrete it claims to be on the “losses”.

UK GDP, and UK GDP per head – a comparative look

Next, let us look at the UK’s comparative position in terms of changes in GDP and GDP per head over time. The next two charts look at the UK’s rate of change (annual percentage) – first against, other EU countries, and second, against a group of non-EU countries, including the EEA/EFTA countries, Norway and Switzerland.

And for the UK compared to non-EU countries:

In the first chart, we see that the UK generally had a lower rate of annual change in GDP than EU members prior to joining, but thereafter the picture is more mixed. During some of the Thatcher years, UK GDP rose more rapidly, but the falls were deeper and a little longer. In the late 90s and early 2000s, the UK generally fared better, but did badly at the trough of the crisis. Finally, the UK was fortunate not to be a Euro area member as the zone’s crisis deepened.

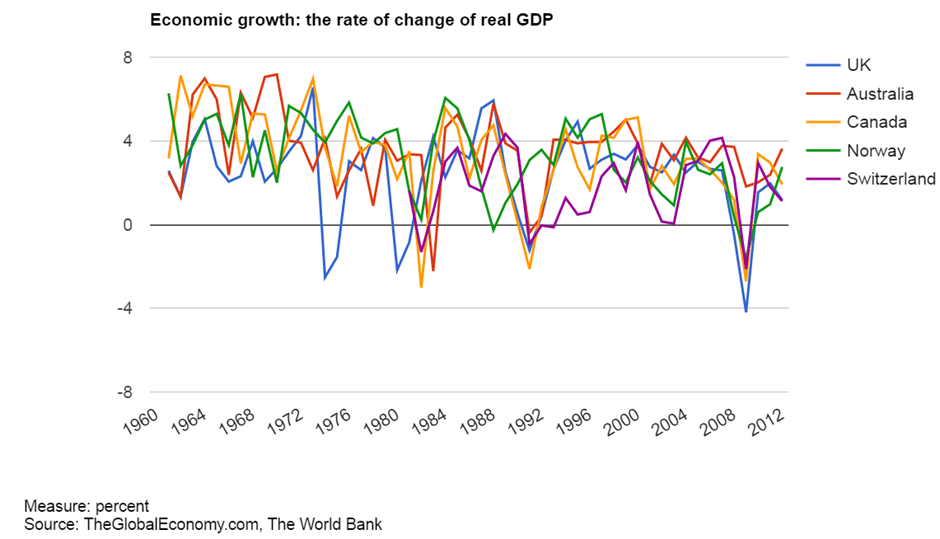

When compared with non-EU countries, we find that the UK tracks fairly closely with Australia, Canada and Norway over time, save that it is prone to worse and earlier recessions. But Switzerland, for all of its wealth, has fared generally more poorly than the UK or other countries since its data begins in about 1980.

Looked at from the perspective of GDP per head of population, I again offer two charts. The first looks at comparative GDP in constant dollar terms (to do away with exchange rate fluctuations), and the second looks in dollar parity purchasing power.

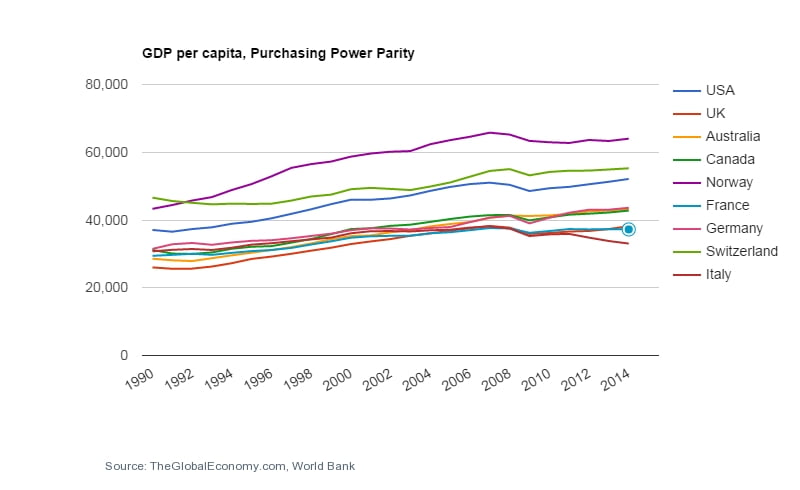

Here we see that the EEA-EFTA countries, Norway and Switzerland, have by far the highest GDP per head, on either basis. In the first chart, GDP per head in constant dollars, the UK can hardly be separated from non-EU countries, Australia and Canada, over many years, but in terms of EU countries is a little ahead of France and Italy but on a par with Germany. When compared in PPP terms, however, the UK is close to the bottom, running in tandem with France, and only Italy falling behind. A grouping of Australia, Canada and Germany are well ahead, and Norway and Switzerland (as well as the USA) again maintained their long-term lead.

My conclusion from these charts is that, overall, it is hard to see that membership of the EU has any particularly strong impact one way or another. The differentials visible in 1990 are broadly still in place today. True, the UK started at the bottom in 1990 in PPP terms, but having caught up with France and Italy, made little headway after 2005. Each country with an “advanced economy” has found its own way of surviving in the world, save perhaps for Italy which – locked into the Eurozone for which it is ill-suited economically – has fallen back badly. Italy is of course a warning that even advanced economies can slip backwards.

The UK and Trade

The Treasury document argues

“In the long term, greater openness to trade and investment boosts the productive potential of the economy. Openness increases competition among firms, allows access to finance from abroad, improves the quality of production inputs, and creates incentives to innovate and adopt new technologies. The HM Treasury analysis estimates the impact on trade and FDI and what this means for productivity and GDP under EU membership and the alternatives. Higher productivity means better quality jobs which lead to higher real wages and household incomes.”

It is not my purpose to deny that much trade brings benefits to citizens and in the productive capacity of a country. Likewise with productive investment that is there for the long-term. But once again, the modelled benefits are hard to see so clearly when one examines the real-life data. And the “free trade” dogma assumes that all kinds of trade are always and everywhere positive – which we increasingly understand is not the case.

Here is a snapshot (2014) of the widely differing position of exports as a percentage of GDP in a set of “advanced” economies (imports are of course broadly similar, allowing for trade deficits and surpluses). Now it is natural that the US – with its vast internal market – would have a much smaller share of GDP attributable to trade, but generally, there is little correlation between the trade density of each, and the actual economic outcomes. There is a greater (but far from strong) correlation between size of population and trade density.

The next chart shows the development of UK exports from 1960 onwards, as a percentage of GDP. It is evident from this that soon after the UK’s entry to the EEC/EU, exports started to play a more important role in the UK economy, moving from around 18-20% earlier to 25-30% thereafter. However, as we have seen, average real annual GDP did not rise during the post-entry period compared to the pre-entry period, so whereas the data shows trade playing a larger role, it does not necessarily follow that a slight reduction in trade would reduce overall economic activity. The fluctuations bear some relation to economic activity but e.g. trade was a smaller proportion in the late 80s/early 90s recession, and a higher proportion in the post-2008 austerity period. This of course is also connected to the current account deficit which has grown in recent years, with a continuing deficit also in the balance of trade.

Yet the Treasury report simply says this about the benefits of trade as a member of the EU:

“Membership of the EU has made it easier to trade both with the EU and the wider world. Trade as a share of national income has risen to over 60% in the past decade, compared to under 30% in the years before the UK joined the EU. The HM Treasury analysis, which is in line with academic research, shows that EU membership increases trade with EU members by around three quarters.”

They do not argue directly here – though it is picked up elsewhere in the paper as we will see – that increased trade leads to – or is at least strongly correlated with – increased GDP, but in fact the correlation is far from strong, and leadsinto complex issues of causation (e.g. it is more likely that increased economic activity causes more trade, rather than vice versa). But the relatonship to GDP is more complex anyway, as an increase in trade deficit leads to a diminution in GDP

The problem therefore is not just the level of trade – and the Treasury report adds the export and import levels together to give the trade percentage of GDP of over 60% – but the balance of trade. If exports fell slightly but imports fell further, then (all else being equal) GDP would increase. In the imports chart below, we see however that imports have exceeded 30% of GDP in 8 years, and recently by significant margins, while exports have only recently – and modestly – reached that level.

Foreign direct investment

The Treasury report says:

EU membership has also made the UK an attractive place to invest and one of the top global destinations for FDI. Almost three quarters of foreign investors cite access to the European market as a reason for their investment in the UK.

There is no reason here to doubt that this is factually true. But again, it does not help us draw conclusions about the impact of leaving the EU, since there is no assessment of data as to how far inward FDI actually tends to increase GDP. Some FDI undoubtedly has a positive effect, not least in counter-balancing the tendency of British capital to invest outside the UK, and in any event capital inflows are in part a corollary of having a large current account deficit.

However, the next chart shows that for most of the period of our EU membership, FDI has been a relatively modest affair – the two exceptions are the late 1990s, and the period just before the great financial crisis. Both these periods are in fact “boom” periods, followed by the dotcom crash first, and the GFC disaster in the second. Since 2008, we have returned to the earlier modest percentages.

The next table, from UNCTAD’s 2012 World Investment Report, shows that the UK had (and has) the largest FDI stock of any EU country, followed closely by France with Germany some way below (but now attracting more than France). The UK’s stock is around one-third of the US’s which makes it very high in proportion.

But once again, there is no evident link between the extent of FDI (as stock or flow) and the development of GDP or GDP per head, and the Treasury does not try to make a data-related link. The report again seems to invite the reader to infer conclusions that are not made explicit, nor the subject of comparative cross-national study.

Since 2011, FDI into the UK has continued to increase – the Treasury report tells us:

“The total stock of inward FDI to EU countries, which includes FDI from other EU countries, was $8.8 trillion in 2013, of which $1.6 trillion (18%) was invested in the UK. This made the UK the largest recipient of FDI in the EU, ahead of Germany and France (with inward FDI stocks of approximately $1 trillion each).”

The figures are hard to tie down, but a very recent OECD paper (“FDI in Figures”, April 2016) tells us that globally

“FDI increases by 25% in 2015, with corporate and financial restructuring playing a large role”.

The UK is here said to have a stock of about $1.2tn, though in 2015, the UK volume dropped by 25% from $52 to $40bn. About 20% of FDI in the UK is in manufacturing, and about 30% in finance and insurance (the rest largely in other services).

It is worth looking at the overall FDI position for “advanced” economies, still from the OECD:

“OECD FDI inflows almost doubled in 2015 (to USD 1 063 billion) compared to 2014, reaching their highest level since the beginning of the financial crisis. However, they remain 19% below their peak level in 2007 (at USD 1 316 billion). They increased by 55% in the first half of the year (to USD 571 billion) from the second half of 2014 and then dropped by 14% (to USD 492 billion) in the second half of the year. The increase in the first half of the year was largely due to record levels of FDI inflows into the United States in the first quarter of 2015 (to USD 200 billion) due to some large cross-border deals.”

This shows that much FDI is for tax and speculative purposes, not serious productive purposes, and second, that the relationship between FDI and increased economic activity is extremely hazy, as 2015 was a year in which global GDP advanced only very modestly (3.1%).

However, the Treasury report seeks to make a link with increased productivity (1.77):

“There is strong evidence that UK trade and investment has been higher as a result of this access to the Single Market. This has increased productivity in the UK. Higher productivity means better quality jobs, and higher real wages and household incomes.”

The problem is, productivity in the UK is far behind most other high-income EU and OECD countries and in recent years has not been growing rapidly, precisely at the time when FDI has been rapidly increasing and is far greater than elsewhere. Either the increases have not had the claimed impact on productivity, or the rest of the economy is in the direst condition…

Can we quantify the benefits of trade and FDI?

The Treasury report does try to cite researchers who have sought to quantify, in terms of GDP per head, the benefits of increased trade, though we get into causation/circularity arguments (did trade increase because of economic activity increasing, or vice versa?).

The clearest claims are this:

“Frankel and Rose (2000) estimate that a 1 percentage point increase in the trade to GDP ratio increases GDP per capita by 0.17% to 0.33%”.

Feyrer (2009) uses the relative cost of transporting goods via air following changes in transportation technology as a proxy for trade costs, estimating that a 1% increase in the growth rate of exports is associated with a 0.5% to 0.75% increase in the growth rate of GDP per capita.”

Taking the first, if we assume an increase in GDP per capita, and that the increase in trade is 20 percentage points (from approximately 40% in 1972 to 60% today) then GDP per head will be at least 6% higher than it would have been if trade had not increased. Yet we recall that since entry to the EU, the average rate of annual increase of GDP is actually slower than in the pre-membership period. And almost the same percentage of GDP was reached by 1976 (around 56%), so already by the mid-70s the increase in GDP would have been solely due to the trade effect!

And in recent years, as increases in GDP per head have almost stagnated, it means that barring the change in trade from 2009, GDP per head would have plummeted. This surely exaggerates the effect of trade changes compared to all other economic considerations by a large margin, and does not seem borne out by the pattern of the GDP data (including pre-EU data) set out in earlier charts.

The second point (Feyrer) is more difficult to assess. What the author actually claims is this:

“An increase in the volume of trade of 10 percent will raise per capita income by over 5 percent.”

Therefore the claim is that an increase in trade of 20% will raise per capita income by over 10%. Once again, this is extremely hard to reconcile, at such a level, with actual UK GDP per head data and trends over time. However, he is talking of volumes of trade as such, not as a percentage of GDP, and he argues that Frankel and Rose’s conclusion is too high. Feyrer also raises the causation issue, positing that trade may be a proxy for a set of economic integration factors.

The next chart shows the annual percentage change in exports for France, Germany, Denmark, UK and the USA, and demonstrates no clear pattern between change in exports, and change in GDP per head. For example, France fell behind the UK in export increases from 2001 to 2009, but has been ahead of the UK since at a time when its economy has been even weaker. (Germany’s rate of increase of exports has been higher generally, and Denmark’s lower, which gives at least some support to Feyrer’s thesis). NB this chart includes services, which are not relevant to Feyrer’s methodology.

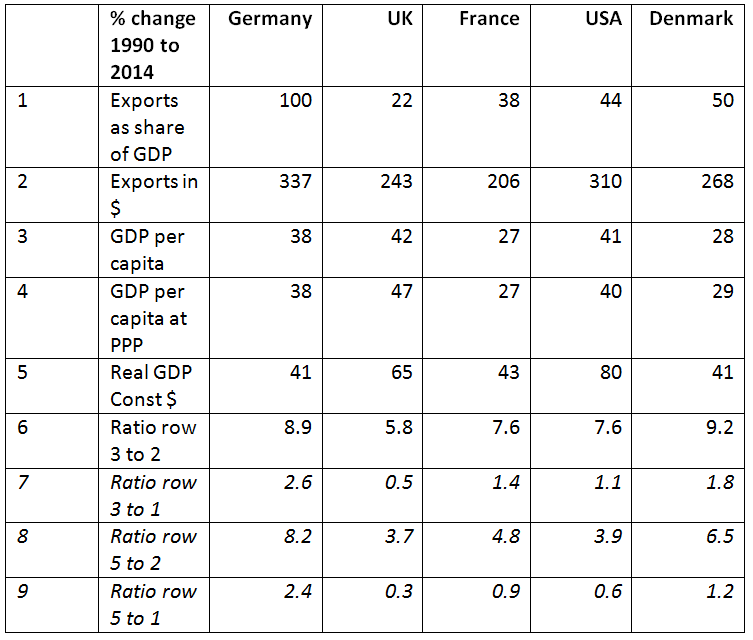

As a simple exercise, I have looked at the trade and GDP data for the UK, France, Germany, USA and Denmark, taking 1990 and 2014 as the two dates. I have calculated the percentage changes in trade and GDP and then looked at the ratios that flow. Since this depends on the years selected, I do not claim it has any scientific force, but it does cover a 25 year period during which the EU single market has largely been operative. The curious result is that the UK is the economy in which trade increases appear to have had the lowest impact!

The UK’s GDP per head has risen more than any othre country’s over the period, but the increase in exports as a percentage of GDP was less than elsewhere, and the rise in exports (in USD) was less than in the other comparators bar France. Germany’s exports had to work much harder to achieve its increase in GDP per head!

Demand in the economy

The Treasury analysis is narrow in its focus. Above all, and true to its commitment to self-defeating austerity, it does not consider the issue of demand in the economy. Its only purpose in the report is to compare hypothetical trade scenarios, and to a lesser extent FDI scenarios, without considering other possible developments in the UK economy that could raise national income and develop wider economic activity. A major “plus” in the UK economy since 2008 has been the development of business-related services, but many other areas have tended to be weak, including of course manufacturing and industrial production as a whole.

Over a long period, the key weakness of the UK economy has been the low level of investment. Whether in or out of the EU, increasing capital investment as a proportion of the economy is necessary and the most reliable way of maintaining strong economic activity.

The chart below shows just how far we are, and have been since about 1990, behind all comparator countries. The issue is overall investment, public and private, not just (or mainly) foreign investment. The Treasury report slips in that it is investment, not foreign investment as such, that is the key to productivity but refuses to draw a wider conclusion:

“Access to the Single Market affects the incentives of businesses to invest in the UK, both for domestic firms and foreign firms. This matters because investment in the economy is a key determinant of economic output and productivity growth.”

The specific added-value of foreign over domestic investment can exist, as the Treasury report says:

Evidence suggests that FDI can increase local productivity by influencing the composition of the economy and through positive knowledge spillover to domestically-owned firms.”

But this does not affect the fact that domestic investment is even more important. And the role of the public sector is likely to be crucial in building our next-generation infrastructure, and in kick-starting and supporting private investment. There will also assuredly be a positive multiplier effect from such a programme.

Conclusions

In the end, I share just a little of the Treasury’s perspective, though I do not share their economic philosophy nor propagandistic approach. It is hard to see how and why Brexit – assuming the same free-trade philosophy of the successor government as of the present government – should lead to any better outcome in terms of trade, at least for quite a long time, and some good reason to believe that the situation would be worse. It is not as if the UK is heavily regulated in terms of labour protection. On the contrary, the OECD tells us that we are (with the US and Canada) in the bottom 3 most deregulated countries in the world as regards employment protection. And so on.

Moreover, a “Leave” vote would assuredly lead to a period of uncertainty in terms of FDI and of domestic private investment. The negotiation inside the EU will last for at least 2 years, to be followed by any residual uncertainty about what is to happen. This would need to be countered by a large-scale public investment programme – but it is hard to see that the new right-wing Brexit-negotiating government would have this on its agenda. It is likely to be even more economically orthodox and deficit conscious than the Cameron-Osborne government!

All this might not matter so much if it were not for the trade and current account deficits. We have to consider that the pound would rapidly and significantly fall in value, and that the trade gap could become even larger if this sucks in more imports. (Of course, other things being equal, it should boost exports, but this may be affected by uncertainty).

So if we have a fall in private investment which is not matched and indeed surpassed by an increase in public investment, a tough recession seems likely. A government committed to a more “autarkic” policy might be able to deal with the situation, but that is not what we will have. I do not think that the current slowdown in the UK economy is caused by the Referendum campaign’s shadow, but it does seem that a decision to Leave would coincide with an already difficult situation.

I have also sought to show from the various charts that – in or out of the EU – so-called advanced economies have for the most part found their own economic way of being-in-the-world, and that over time they have tended to progress at relatively similar paces. I have little doubt that the UK can survive outside the EU, and find in due course a sustainable path. But for a while, it may be hard going. And in a few cases – take Italy to date – there has been a serious sustained decline. It is going to be hard indeed for a single country to change the economic paradigm, which is why we need to work together.

So to friends who see the economic faults of the EU and especially the Eurozone, and are thinking how to vote, I would argue that our task is to work in solidarity, to work for unity to change the EU’s policies in a progressive and democratic direction. My vote to remain will be based on the opposite economic grounds to the “Remain” campaign’s.

And a Happy Europe Day to one and all!

This article was slightly edited and amended by the author on 11th May.

Nice data, it shows that EU membership has little effect on UK economy except, perhaps, a small reduction in GDP growth.

The only economic argument you have advanced for staying in the EU is that the uncertainty post referendum will damage the economy. What happened? The uncertainty was maximised by not invoking Article 50 (as the media say, no one knows what will happen) yet the UK economy has been robust, probably exceeding 0.3% growth in Q3.

Perhaps in future you will stick to what the data predicts – little difference IN or OUT – instead of trying to bring an "uncertainty" rabbit out of the hat at the end of the article.

One Response

Nice data, it shows that EU membership has little effect on UK economy except, perhaps, a small reduction in GDP growth.

The only economic argument you have advanced for staying in the EU is that the uncertainty post referendum will damage the economy. What happened? The uncertainty was maximised by not invoking Article 50 (as the media say, no one knows what will happen) yet the UK economy has been robust, probably exceeding 0.3% growth in Q3.

Perhaps in future you will stick to what the data predicts – little difference IN or OUT – instead of trying to bring an "uncertainty" rabbit out of the hat at the end of the article.