The 2016 Euro Convergence Reports from the European Central Bank (ECB) and the European Commission, published today, provide stark evidence of an institutionally embedded bias in favour of deflation. They have taken the three EU Member States suffering from the most severe annual deflation as their benchmarks for “best performers” in the EU for “price stability”.

In doing so, they have applied the wrong legal test on the EU Treaty meaning of “best-performing” in Article 140 (see below) – and one that goes against the ECB’s own clear statement that deflation is “inconsistent with price stability”. On this occasion, the use of the legally wrong test of “best performers” affects their assessment of Sweden (which narrowly fails the price stability test). Moreover, the ECB and Commission have set a dangerous deflationary precedent for all future assessments, and their methodology must not be allowed to stand without challenge.

The Reports should therefore be rejected in their present form by the European Council (representing the Member States), and the European Parliament (which must by law be consulted) should advise the Council not to accept them as they stand.

The story in brief

The ECB and Commission are required by Treaty to publish a Convergence Report every two years, assessing how far non-Euro EU Member States (apart from the UK and Denmark, which have their respective opt-out) have got in meeting their legal obligation to move towards satisfying the convergence criteria for joining the Euro.

In sum, there are four main “convergence criteria” to be met in order to join the Euro, of which “price stability” comes at the top of the list. This depends on comparing the “candidate” with the average of the three “best-performing” states in terms of price stability.

What the ECB and Commission have done, however, is to take the average of the three states (excluding those they deem to be subject to exceptional factors) which have had the highest rate of deflation over the last year, and compare the non-temporary inflation/deflation rate of each “candidate” with these. To meet the legal “convergence” test on price stability, the Euro candidate state must not have inflation of more than 1.5 percentage points above the average of the three best performers for stability.

Using the ECB’s and Commission’s deflationary “best performers”, the maximum they come up with is 0.7%. This comes from adding the 1.5% leeway to the average deflation of the alleged “best performing” states at -0.8%. What they should have done is taken the average of the three states with the greatest “price stability”, i.e. at or just above zero inflation. While we do not have access to the precise data the Commission have used, it seems probable that the correct comparators would have annual inflation rates of between 0% and 0.4%.

This means that even adding 1.5% to the average, one would still not get a convergence “ceiling” above the ECB’s 2%. If the institutions had done this correctly, Sweden would have qualified to join the Euro under the heading of price stability (though once again deliberately failing on other tests!), since its relevant inflation rate is considered to be 0.9%.

This perverse methodology, based on a benchmark of three least price-stable states, is patently contrary to the wording of the Treaty and the Protocol, and leads to defining a state with an inflation rate of less than 1% as non-convergent!

The legal position

The legal requirements are as follows.

Article 140(1) of the Treaty on the Functioning of the European Union:

“The reports shall also examine the achievement of a high degree of sustainable convergence by reference to the fulfilment by each Member State of the following criteria: — the achievement of a high degree of price stability; this will be apparent from a rate of inflation which is close to that of, at most, the three best performing Member States in terms of price stability…

The four criteria mentioned in this paragraph and the relevant periods over which they are to be respected are developed further in a Protocol annexed to the Treaties…”

Article 1 to Protocol 13 to the Treaty, on the convergence Criteria, adds this in relation to the criterion:

The criterion on price stability referred to in…Article 140(1)…shall mean that a Member State has a price performance that is sustainable and an average rate of inflation, observed over a period of one year before the examination, that does not exceed by more than 1 ½ percentage points that of, at most, the three best performing Member States in terms of price stability. Inflation shall be measured by means of the consumer price index on a comparable basis taking into account differences in national definitions.

The criterion, therefore, against which best performance is to be judged is price stability. Neither Article 140 nor the Protocol define this term further, so it must be given its natural meaning. Choosing the states with the greatest downward price instability is a legally unjustifiable way of interpreting the term.

The ECB has however defined the meaning of price stability as follows (this is from its website):

While the Treaty clearly establishes the primary objective of the ECB, it does not give a precise definition of what is meant by price stability.

The ECB’s Governing Council has announced a quantitative definition of price stability:

“Price stability is defined as a year-on-year increase in the Harmonised Index of Consumer Prices (HICP) for the euro area of below 2%.”

Moreover, from the same source we read:

Symmetry

By referring to “an increase in the HICP of below 2%” the definition makes clear that not only inflation above 2% but also deflation (i.e. price level declines) is inconsistent with price stability. [my emphasis]

It continues with a passage on “Reasons for aiming at below, but close to, 2%” i.e. the inflation target of its monetary policy.

What today’s Convergence reports say

Now, back to today’s reports as they deal with “price stability”. First, this is what the ECB says:

In the context of this report, the ECB applies the Treaty provisions as outlined below.

First, with regard to “an average rate of inflation, observed over a period of one year before the examination”, the inflation rate has been calculated using the change in the latest available 12-month average of the HICP over the previous 12-month average. Hence, with regard to the rate of inflation, the reference period considered in this report is May 2015 to April 2016.

Second, the notion of “at most, the three best performing Member States in terms of price stability”, which is used for the definition of the reference value, has been applied by taking the unweighted arithmetic average of the rates of inflation of the following three Member States: Bulgaria (-1.0%), Slovenia (-0.8%), and Spain (-0.6%). As a result, the average rate is -0.8% and, adding 1½ percentage points, the reference value is 0.7%. It should be stressed that under the Treaty a country’s inflation performance is examined in relative terms, i.e. against that of other Member States. The price stability criterion thus takes into account the fact that common shocks (stemming, for example, from global commodity prices) can temporarily drive inflation rates away from central banks’ targets.

The inflation rates of Cyprus and Romania have been excluded from the calculation of the reference value. Price developments in these countries over the reference period resulted in a 12-month average inflation rate in April 2016 of -1.8% and -1.3% respectively. These two countries have been treated as “outliers” for the calculation of the reference value, as in both countries inflation rates were significantly lower than the comparable rates in other Member States over the reference period and this was due, in both countries, to exceptional factors.

The European Commission report, along very similar lines, after citing Article 1 of the Protocol, says:

The requirement of sustainability implies that the satisfactory inflation performance must essentially be attributable to the behaviour of input costs and other factors influencing price developments in a structural manner, rather than the influence of temporary factors. Therefore, the convergence examination includes an assessment of the factors that have an impact on the inflation outlook and is complemented by a reference to the most recent Commission services’ forecast of inflation.

Related to this, the report also assesses whether the country is likely to meet the reference value in the months ahead. The inflation reference value was calculated to be 0.7% in April 2016, with Bulgaria, Slovenia and Spain as the three ‘best-performing Member States’ [Footnote 7 states “The respective 12-month average inflation rates were -1.0%, -0.8% and -0.6%].

It is warranted to exclude from the ‘best performers’ countries whose inflation rates could not be seen as a meaningful benchmark for other Member States. [Footnote 8: “The use of the term ‘best performer in terms of price stability’ should be understood in the meaning of Article 140(1) TFEU and is not intended to represent a general qualitative judgement about the economic performance of a Member State”.]

Such outliers were in the past identified in the 2004, 2010, 2013 and 2014 Convergence Reports. At the current juncture, it is warranted to identify Cyprus and Romania as outliers, as their inflation rates deviated by a wide margin from the euro area average and including them would unduly affect the reference value and thus the fairness of the criterion10. In case of Cyprus, deeply negative inflation mainly reflected the adjustment needs and exceptional situation of the economy. In case of Romania, it was mainly due to large VAT rate reductions. Against that background, Bulgaria, Slovenia and Spain, the Member States with the next-lowest average inflation rates, are used for the calculation of the reference value.”

The Commission’s report seeks to defend its methodology as follows:

The notion of ‘best performer in terms of price stability’ is not defined explicitly in the Treaty. It is appropriate to interpret this notion in a non-mechanical manner, taking into account the state of the economic environment at the time of the assessment. In previous Convergence Reports, when all Member States had a positive rate of inflation, the group of best performers in terms of price stability naturally consisted of those Member States which had the lowest positive average rate of inflation. In the 2004 report, Lithuania was not taken into account in the calculation of the reference value because its negative rate of inflation, which was due to country-specific economic circumstances, was significantly diverging from that of the other Member States, making Lithuania a de facto outlier that could not be considered as ‘best performer’ in terms of price stability.

In 2010, in an environment characterised by exceptionally large common shocks (the global economic and financial crisis and the associated sharp fall in commodity prices), a significant number of countries faced episodes of negative inflation rates (the euro area average inflation rate in March 2010 was only slightly positive, at 0.3%). In this context, Ireland was excluded from the best performers, i.e. the only Member State whose average inflation rate deviated by a wide margin from that of the euro area and other Member States, mainly due to the severe economic downturn in that country. Outliers were also identified in 2013 (Greece) and 2014 (Greece, Bulgaria and Cyprus). At the current juncture, it is warranted to identify Cyprus and Romania as outliers, as their inflation rates deviated by a wide margin from the euro area average, driven by country-specific factors that limit their scope to act as meaningful benchmarks for other Member States. In case of Cyprus, deeply negative inflation mainly reflected the adjustment needs and exceptional situation of the economy. In case of Romania, it was mainly due to large VAT reductions. In April 2016, the 12-month average inflation rate of Cyprus and Romania were respectively -1.8% and -1.3% and that of the euro area 0.1%.

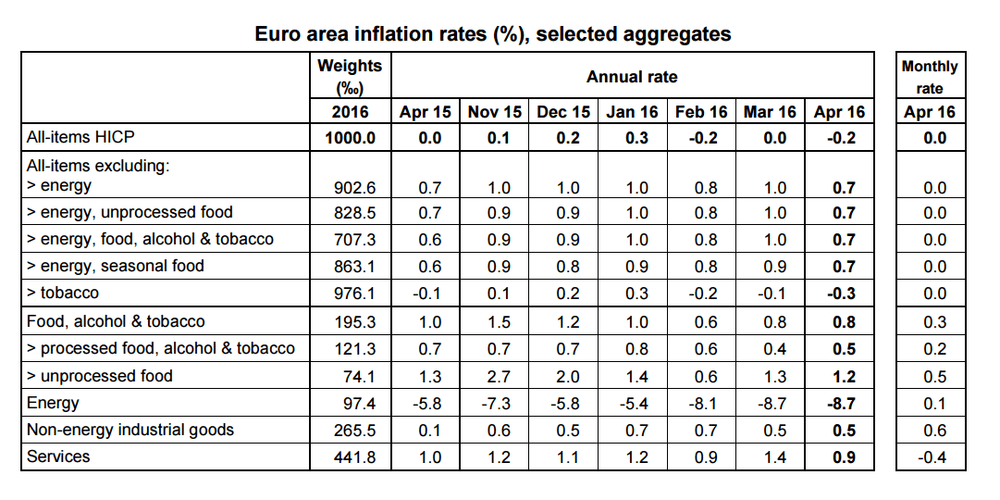

I cannot find any explicit table setting out the Commission’s calculations for inflation by country after discounting the influence of “temporary factors” like the fall in energy costs, but here is the table from the press release of Eurostat which shows the overall HCIP inflation for April 2916, and the annual figure excluding energy etc. The overall figure has hovered around zero, while the figure excluding energy is around 0.7-1%. It is almost certain that the three most “price stable” countries will be well below this level, e.g. between 0% and 0.4%, making an average of say 0.2%. This would make the correct reference rate around 1.7%, a whole percentage point higher than the institutions’ wrong test.

source: Eurostat

But while it appears that the Commission used the same methodology in 2010, this does not affect the argument that what they have done now is wrong in law. Had they taken the three states closest to zero (whether in tiny inflation or deflation), one could understand the methodology. But to take precisely those that are furthest (downwards) from zero is a patent disregard for the clear wording of the Treaty and Protocol.

No, through today’s Reports, the Commission and the ECB have told the world that for them, the higher the rate of deflation (excluding exceptional factors), the better they consider a Member State’s ‘performance’ in terms of price ‘stability’. This is bad law, and even worse economics.

Annex:

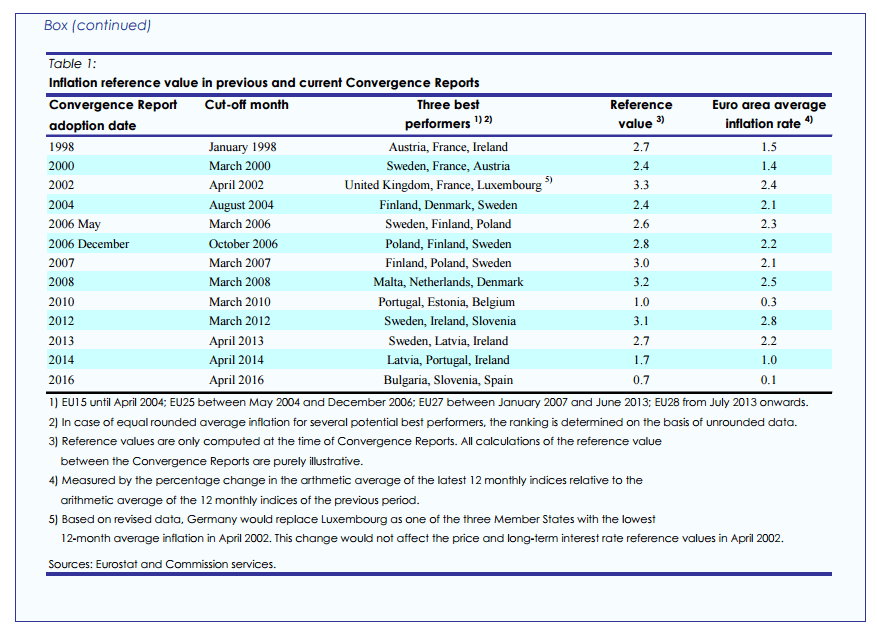

For information, here from the European Commission’s Convergence Report is a table sahowing the countries and the inflation rates applicable in relation to previous such Reports. Note that there was also deflation in 2010 which appears to have affected the choice of best performers, but this was in the context of an acute (as against today’s chronic) crisis:

One Response

A clear case of Humpty Dumpty economics – Price stability is what I choose it to mean – neither more nor less!