On 7th January, Chancellor George Osborne announced that this year, the economy was “mission critical”. Mission critical to exactly what, he did not say. But it was so important that he used the phrase four times in one speech. Last Friday, the Chancellor finally admitted that the economy was “smaller” than he had expected, and confessed that he is now looking to make even deeper cuts than so far programmed. He told the BBC:

“We may need to undertake further reductions in spending because this country can only afford what it can afford and we will address that in the Budget. We’ve just had figures that show the economy is smaller than we thought in Britain, and we also know that global risks are growing and Britain is not immune to those things.”

In fact, while global risks may be growing, their intensification has little or nothing to do with the recent difficulties the Chancellor faces, as he prepares next month’s budget (16 March). They were already there last November, at the time of the Autumn Statement. At that time, he was rescued – as if by magic – from a difficult political situation (over working tax credits) by some strangely over-optimistic assumptions from the Office for Budget Responsibility.

Now, he has no place to hide. It’s a case of severe mission failure.

On 17th January, we pointed out that the government and OBR numbers were in trouble – and called our article “Beware Budget 2016”. Our assessments made then look like being spot on. As we know, the economy is unbalanced anyway, with industrial production and construction in the doldrums, while many service sectors are doing reasonably well (notably retail, information and communication, some business services, and real estate services).

But for the government, perhaps the biggest problem – the usually hidden side of deflation – is that nominal GDP (current price GDP) has been slowing rapidly. This affects the level of actual cash spend in the economy, and crucially, affects the tax take for the government. So while people are buying more stuff, for example, their actual spending is not much more than the previous year – so VAT receipts have not increased much.

The impact of low nominal GDP

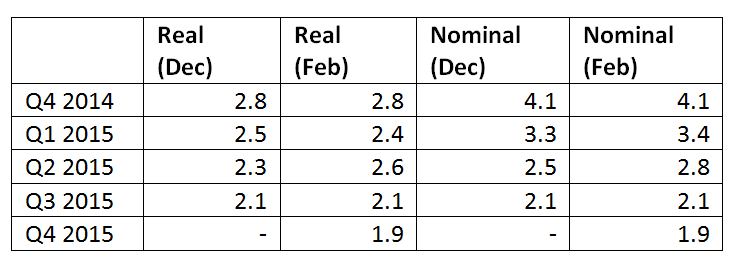

When the Q3 2015 figures were published, we highlighted the very unusual fact that nominal GDP had gone up by no more than “real” GDP (i.e. allowing for inflation). Both increased, year on year, by 2.1%. This week saw the latest figures for Q4 published by ONS – and show that once again, nominal and real GDP went up, year on year, by the same amount – this time 1.9%. (The last time nominal GDP went up by no more than real GDP for two successive Quarters was back 55 years ago, in 1960).

When nominal GDP is less than expected, due to a slowing economy and deflation, this has another consequence – it increases the burden (or “value”) of debt. Thus even if the government were to borrow no more this year in cash terms than the OBR had previously forecast, the size of the deficit and of the total debt stock, measured as proportions of GDP, increase. That is because the total (nominal GDP) is lower than anticipated. In fact, it now looks likely that public sector borrowing in 2015/16 will come in about £4-5 billion over the amount forecast at the start of the year by OBR, and left unchanged in its November Outlook report.

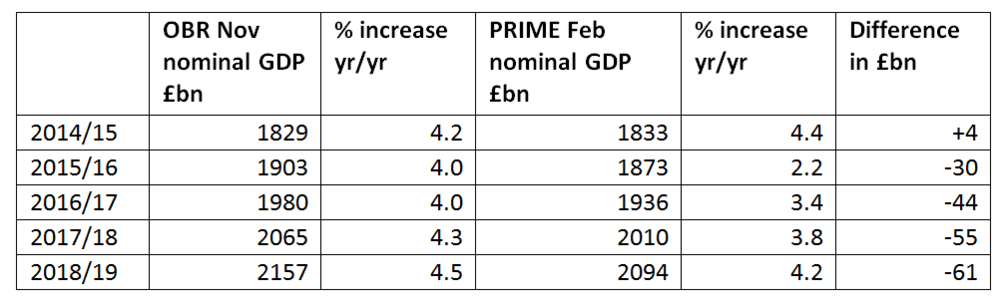

We calculate that (assuming that nominal GDP in Q1 2016 is around 0.6% above Q4 2015) nominal GDP for the financial year 2015/16 will end up around £30 billion, or over 1.5% of GDP, below the OBR’s forecasts.

Moreover, the combination of slightly higher borrowing and lower nominal GDP means that – in our estimation – the current budget deficit for this financial year will rise from the OBR-projected 2.1% to 2.3% of GDP, and the overall deficit – which includes capital investment – from 3.9% to 4.1%. This will also put the borrowing figures for future years in doubt.

Our anti-deficit Chancellor breaks deficit record

This means that the very Chancellor who has inveighed against deficits (even for investment!) so loudly and so long has overseen our economy for 6 years without getting the deficit below 4% of GDP, and without getting the current budget deficit below 2.2%. This is a record for any Chancellor. It demonstrates the economic nonsense of trying to get rid of deficits by austerity; or alternatively, the relative merit (absent a sensible economic policy) of keeping deficits going if you want to avoid the even worse performance of Eurozone countries whose economies have had even more austerity thrust upon them.

Back in our January article, we included two tables. The first showed the evolution of real and nominal GDP by quarter (compared with the same quarter a year before) since Q4 2014. The second showed the OBR’s estimate of nominal GDP through to 2017/18. We have updated these and rolled them forward.

Table 1 – ONS estimates of GDP (December 2015 and February 2016)

Looking further at changes in nominal GDP, we recall that the OBR in their November 2015 Outlook said:

“We expect annual nominal GDP growth to fall back from 4.7 per cent in 2014 to 3.6 per cent in 2015, largely reflecting slower quarterly growth of nominal GDP in the second half of 2014 that affects the annual growth rate in 2015. Nominal GDP growth is then expected to pick up steadily from 2016..”

In fact, the latest (February) ONS figure for nominal GDP growth for the whole of 2015 is 2.6%, or one full percent below the late November estimate! We feel it unlikely that any pick-up from 2016 on will be anything like as strong as OBR estimated.

Table 2 – OBR estimates of fiscal year nominal GDP (November 2015), plus PRIME approximate estimates (February 2016)

All OBR figures are from the OBR Databank. The PRIME figures for 2014/5 and 2015/6 are based on ONS latest data with assumption of Q1 2016 q/q increase of 0.6%