The Assertion

Even before Corbyn launched the Labour Manifesto, the Institute of Fiscal Studies launched its critique of Labour tax policies, asserting that Labour’s proposed tax increases were not limited to the richest,:

“The truth is of course that in the end corporation tax is paid by workers, customers or shareholders so would affect many in the population”.

On the BBC Shadow Chancellor John McDonnell politely rejected the IFS critique, which in essence asserts that the corporate income tax is not progressive. Well he should, because the “initial reaction of IFS researchers” (as they entitle their article) is wrong about the corporate income tax.

For the public this argument may seem obscure. Why is there disagreement over something as apparently obvious as who pays a tax? Surely it is a question of tracing the money flow. The question proves more complicated on inspection. However, when considering the complications we must not lose sight of the central issue for every tax, is it progressive?

The Reality

The general rule is clear. Indirect taxes, such as VAT, are regressive. They fall more heavily on lower income groups because they tax spending, and as incomes rise expenditure declines as a share of income. High income groups save and low income groups do not, with savings in the middle almost entirely mortgage repayments (which are not subject to VAT).

Further, it is extremely difficult to make indirect taxes progressive beyond relatively unimportant examples of taxing luxury goods that raises little revenue. Also, indirect taxes can be “shifted”; that is, the group that actually pays the tax can by increasing prices shift the payments to the purchaser of the VAT covered item. Market power determines the extent to which a company can do this. An energy company will have considerable scope for tax shifting, since due to their heating systems households find it difficult to switch from electricity to gas (and vice-versa) in the sort run. On the other hand, producers and sellers of generic consumption products such as common household wares may find it difficult to pass on tax through higher price without debilitating loss of sales.

By contrast, direct taxes on household incomes, corporate profits and property are progressive. No serious argument exists that people or households can shift the personal income tax. The most superficially plausible argument maintains that income taxes discourage working time, thus lowering the supply of labour and pushing up wages and production costs. We find little empirical evidence to support this assertion.

Targeting higher income groups for additional tax proves a relatively easy technical task. The policy stated in the Labour manifesto to limit income tax increases to the richest 5% of households implied in 2018 raising the tax rate for those with an average annual income in excess of approximately £75-80,000. In 2018 that would have affected 1,356 thousand households and 3,326 thousand people.

In that year the richest 5% paid slightly over half of personal income tax, with the marginal rate of tax at 40% above £50,000 then 45% above £150,000 (41 and 46% in Scotland). Current tax rates on the highest incomes fall far below the 83% that applied in the 1970s, a rate well above the 70% proposed for the richest in the current Labour Manifesto. In the Manifesto, a 45% rate would begin at £80,000 and 50% at £125,000. The latter amount is slightly above the lower boundary for the richest 2%, and the former above but close to boundary for the 5%.

While the income tax may be evaded but not shifted onto others, shifting of a property or more generally wealth tax is specific to each tax and defies generalization. For example, householders will find it nigh impossible to shift their tax, while landlords can to some extent pass tax on to tenants depending on the nature of the rental market. A 2016 IFS report shows that property tax raises relatively little revenue in Britain.

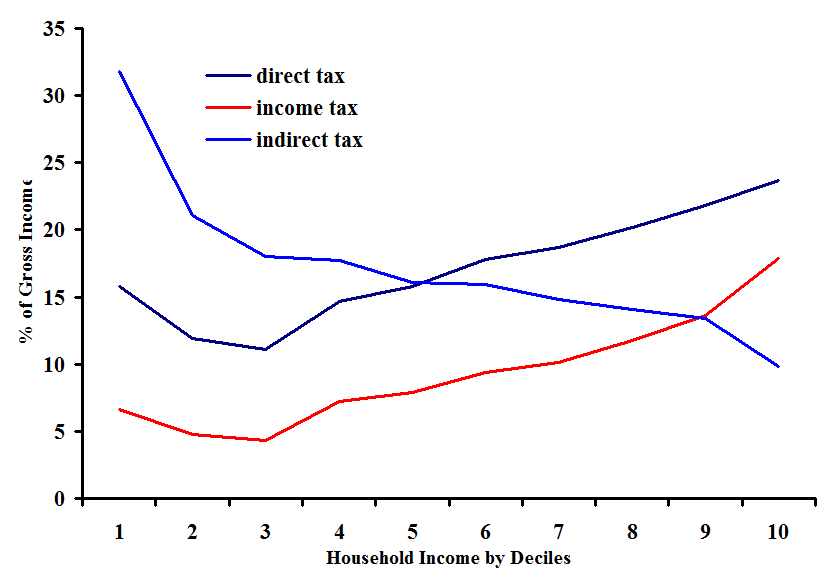

The chart below shows the actual tax payments by households by level of income measured by deciles, with the lowest tenth of income receivers listed first through to the highest. The chart verifies our generalizations. Indirect taxes prove unambiguously regressive. The poorest ten percent pay over 30 percent of their gross (cash) income as indirect tax, falling continuously to 9.8% for the richest 10%. For all direct taxes and the income tax shares fall slightly from the first to the second decile, and again from the 2nd to the third, and then rise continuously.

All Direct, Income & Indirect Taxes, Share of Gross Income by Income Decile, 2017-18

Notes: Deciles are households ranked in ascending order by incomes. The average number of households in each decile is 2.711 million. Source: Office of National Statistics.

Now, we come to the matter of greatest contention – who pays the corporate income tax? Is it the case as IFS “researchers” contend, that the “corporation tax is paid by workers, customers or shareholders so would affect many in the population”? The statement is true, only due to its extremely vague choice of words, and is seriously misleading. We can begin with the most obvious and non-controversial impact, on shareholders. Increases in the corporate income tax by definition lower corporate profits after tax, implying lower dividend payments.

As a factual matter UK dividend recipients are few in number. To quote the Financial Times, “overwhelmingly shares are owned by foreigners and various institutions who manage money on behalf of their clients”. To be specific, in 2016 individuals in the UK held only 12.3% of the shares of UK-based companies (those falling under UK tax law). Notwithstanding the narrow ownership of shares, some might argue that taxing corporate profit harms the many holding private pensions, which invest in the stock market.

The actual numbers are quite small. For all households private pensions account for less than 5% of annual income flows, of which shares themselves generate far less than half. The likelihood that increased corporate tax rate would have a substantial impact on pension payments either for the number of recipients or for payment per recipient is very low.

The assertion that increases in the corporate income tax would be paid by employees is if anything less credible than the stockholder argument. Corporations cannot directly charge employees for the tax they pay. The mechanism that the IFS have in mind must be indirect, through wages levels, that higher corporate tax payments by reducing corporate profits reduce potential wage increases. This is unlikely to be important in the UK current context.

Across companies the relative bargaining power of employees and employers determines wage outcomes. Since the crash of 2008 private sector real wages have grown very slowly and remain below their pre-crash level. These were years during which the corporate tax rate fell from 28% to 19% (shown in a graph from Trading Economics). If as IFS believe higher corporate tax rates depress wage growth, then lower rates should have increased wage growth, for which there is no evidence. In the abstract, corporate profitability is one of many factors influencing wages changes. It does not appear as an important influence in the UK in recent years.

Equally unconvincing is the IFS suggestion that “customers” pay the corporate income tax to any substantial amount. Several of the largest corporations do not directly charge their retail customers, for example Google, Facebook and suppliers of business services. Any link to customers would be very indirect indeed. More generally, market conditions determine the ability of corporations to pass tax increases on to customers. The IFS with its microeconomic focus should be aware that generalizations about market conditions across the private economy are not reliable.

The Evaluation

IFS “researchers” chide Labour for its mendacity:

“If you want to transform the scale and scope of the state then you need to be clear that the tax increases required to do that will need to be widely shared rather than pretending that everything can be paid for by companies and the rich.”

That is, in practice Labour’s tax plans will not be limited to the rich as claimed, but widely spread.

It is factually correct that Labour’s proposed income tax increases for those earning £80,000 or more would affect the richest 5%, and cannot be shifted only evaded. By any reasonable assessment, the proposal to raise the corporate income tax will fall overwhelmingly on retained earnings and shareholders who are overwhelmingly in the richest 5%, and not on employees and customers.

The IFS critique of Labour tax proposals is incorrect. The Labour proposals do not pretend that companies and the rich will carry the burden of increased taxes; they mean that in practice.

2 responses

This is not just intellectually dishonest, it fundamentally misrepresents what the IFS says about Labour’s policy.

It claims the IFS " in essence asserts that the corporate income tax is not progressive" because it says that the tax is paid by real people.

Firstly, the should-be-uncontroversial claim that taxes are ultimately incident on real people (consumers, workers, shareholders, in some proportion) doesn’t on its own say anything about whether a tax is progressive or not. It depends on where the various groups of people are in the income (or wealth or consumption) distribution, and the share borne by these different groups. The statement by the IFS doesn’t make any claim about either of these.

Second, if you actually watch what the IFS researchers say in their briefing on the election manifesto, they explicitly say increases in corporate tax would clearly be progressive – just not incident on ONLY the top 5%, which was Labour’s claim -, especially in combination with the spending on things that would be of bigger proportional benefit to lower and middle income households.

So you’ve made a claim which doesn’t follow from your "evidence" and actually ignores what the IFS actually say.

All to allow you to set up an argument as vague and imprecise as I have seen by an errr former "reseacher". You don’t seem to understand how tax incidence works in labour markets characterised by competitive conditions or wage-bargaining over rents, or the evidence on labour supply and taxation. For example, some groups are highly responsive to effective tax rates on earnings – e.g. lone parents and second earners. And the less responsive workers are to taxation (i.e. net wages), the more scope there is for the burden of taxation – personal, corporate etc – to fall on them. Just draw the supply and demand graphs! More mobile/responsive factors are able to shift tax on to less mobile/responsive factors.

None of this is to deny that Labour’s tax proposals would raise revenue, largely from people towards the top of the income (and wealth) distributions. But then the IFS has never denied that – it has just called out Labour (like it calls out other parties) on the very precise claim they made: that only the top 5% would pay extra tax.

Looks like you have thrown the principles of sound science and economics out when you decided to go full partisan propaganda, didn’t you John?

The number of errors and deliberately misleading statistics in this piece are astounding. For example, you say property taxes raise little revenue, Yet the data shows the various property taxes raise roughly 10% of total tax receipts.

Then you talk about the impact of dividends on shareholders – claiming that UK shareholders are of small number so insignificant.

Of course, the 12.3% of UK held, UK owned shares ONLY accounts for the shares DIRECTLY held. It doesn’t include those shares held by institutions on behalf of their clients – so most of the pension industry. Once you factor in that, the true ownership of UK listed shares by UK residents is around 50%. And that doesn’t include the non-listed companies which would also be hit by Labour’s massive tax rises.

Stop lying, please.