By Ann Pettifor

Last month Ann Pettifor was invited to join the ‘Labour Party Policy Review: Making growth work for the poor and generating resources for development’. The overall group was led by Harriet Harman, and the development section was chaired by Rushnara Ali MP.

Below is Ann’s short background note on mobility of capital flows, financial crises & implications for poor countries:

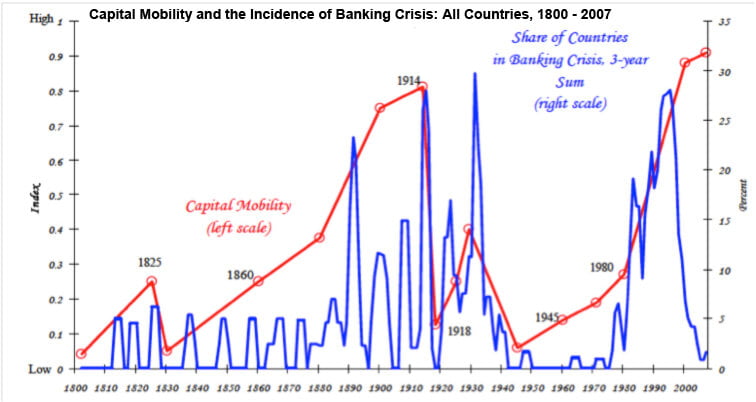

capital_mobility_chart

Chart taken from “This Time is Different: A Panoramic View of Eight Centuries of Financial Crises” by Carmen M. Reinhart, University of Maryland and NBER; and Kenneth S. Rogoff, Harvard University and NBER.

Capital Mobility: what others are saying

“Experience shows that when policies falter in managing capital flows, there is no limit to the damage that international finance can inflict on an economy.”

Yilmaz Akyüz, “Capital Flows to Developing Countries in a Historical Perspective: Will the current Boom End with a Bust?” South Centre:Research Paper 37, March 2011

“..capital flows, it’s like with fire. Fire can be used to turn raw meat into a wonderful steak. But it can also burn your house down.”

Jagdish Bagwhati, Professor of Economics, Columbia University, on Big Think, 17 November, 2007.

“Looking back on the crisis, the US, like some emerging-market nations during the 1990s, has learned that the interaction of strong capital inflows and weaknesses in the domestic financial system can produce unintended and devastating results. The appropriate response is…to improve private sector financial practices and strengthen financial regulation, including macroprudential oversight.”

Ben Bernanke, governor of the US’s Federal Reserve in speech to Banque de France February, 2011.

“So we have to make some choices. Let me be clear about mine: democracy and national determination should trump hyper-globalization. Democracies have the right to protect their social arrangements, and when this right clashes with the requirements of the global economy, it is the latter that should give way.” (Author’s emphasis)

Dani Rodrik. “The Globalization Paradox” Oxford 2011. Page X1X.

“We have been working hard to develop the economy in the past 30 years, but now these elite members of society are fleeing with the majority of the wealth. The loss may be even higher than all the foreign investment we have attracted. It is as if, when the time of harvest comes, we find the fruits have all gone to others’ baskets.”

Zhong Dajun, director of the Beijing Dajun Institute for Economic Observation & Studies, June 8 2011, quoted in Financial Integrity and Development Task Force.

“I have no 10-point programme for making “finance less proud”, as Winston Churchill once put it. I do not believe it will be done just by calling for more macro prudential bank regulation; nor by the so-called Tobin tax on all financial activity.

It is more a matter of recognising, at every point of policy decision, that the free movement of artificially created electronic money across frontiers is not on a par with the free movement of goods and services, let alone more basic human freedoms, and recognising this not only for developing countries but for the so-called advanced ones as well.”

Samuel Brittan, Financial Times, 10 June, 2011. “Good servants can make bad masters.”

Introduction

As the Reinhart/Rogoff chart above clearly demonstrates, capital mobility has been a major cause of global financial instability, in both rich and poor countries. The only period of global financial stability – the so-called ‘golden age’ between 1945 – 71 – was a period of de-colonisation during which capital mobility was constrained [1] and resources for development witnessed sustained poverty reduction in poor countries. Since President Nixon unilaterally dismantled the Bretton Woods System in 1971, capital mobility has intensified, financial crises have multiplied [2] and whole continents endured ‘lost decades’ of development.

After 30 years of frequent and grave crises, control over capital flows (now re-designated as ‘capital flows management’ by the IMF) is now actively discussed, even though debate is limited to controls on inward flows. Debate on controls over outward flows – illicit capital flight that makes it so easy for corporations and elites to export their gains– are still taboo.

The big change came in February, 2010, when IMF staff accepted that ‘capital controls are part of the policy mix’. By April, 2011, the Fund had developed a ‘framework’ to help countries manage capital flows.

This framework was promptly rejected by the G24, led by India and Brazil, for several reasons. First because the IMF was dealing with symptoms, not causes – i.e. the easy money policies of the Federal Reserve. Quantitative easing (QE) was, and is, intended to pump liquidity into the US economy; to allow funds to cascade down through the banking system, for lending to US companies that would, in turn, invest in infrastructure and the creation of US jobs. Instead as Samuel Britten notes above, this ‘artificially created electronic money’ surges across frontiers, chasing speculative gains. This occurs largely because, as noted by Prof. Chick in a recent speech[3] there is neither economic debate about the money supply; nor overt management of the money supply. The IMF shows little interest in the implications for the global money supply of credit-creation by central banks and, in the view of many, turns a blind eye to these de-stabilising activities. The G24 in contrast, demands that a light be shone on the causes of the boom in speculative capital flows.

Second, as Lesetja Kganyago, chairman of the G-24 and director-general of South Africa’s National Treasury told the Wall St Journal: the group opposed the IMF framework because the fund proposed to integrate it into its surveillance program and policy recommendations. G24 leaders – especially those leading some of the world’s biggest democracies – rightly expect to enjoy the same policy autonomy privileges usually reserved for leaders of the G8.

All of this makes a recent paper on the current boom in capital flows by Yilmaz Akyüz of the South Centre timely, comprehensive and insightful. Akyüz is chief economist at the South Centre, Geneva and former director of the Division on Globalization and Development Strategies at UNCTAD, where he edited a range of UNCTAD’s annual reports.

Akyüz begins by noting that there have been three generalised boom-bust cycles in private capital flows since the end of the Second World War: all with devastating impacts on developing and emerging markets. The first started in the late 1970s, and ended with the Latin American debt crisis in the early 1980s. The second started in the early 1990s and was followed by the East Asian financial crisis of 1997/8; and by defaults in Latin America and Russia.

“The third cycle started in the early years of the new millennium and ended in the second half of 2008 with the subprime crisis. This was soon followed by a new boom, the fourth in the post-war era, which started in the first half of 2009 and is continuing with full force as of early 2011.”

Akyüz suggests that this current cycle will most likely end with a reversal in the upswing in commodity prices, because commodity

“markets have become more like financial markets…with several commodities treated as a distinct asset class, attracting growing amounts of money in search for profits from price movements…”

The commodity bubble began with a new financial instrument invented by Goldman Sachs – the Goldman Sachs’ Commodity Index (GSCI) – so argues Frederick Kaufman in the April, 2011 edition of Foreign Policy. Next, commodity price inflation received a boost in 1999, when the US Commodities Futures Trading Commission deregulated futures markets.

“All of a sudden, bankers could take as large a position in grains as they liked, an opportunity that had, since the Great Depression, only been available to those who actually had something to do with the production of our food”

writes Kaufman.

“Since the bursting of the tech bubble in 2000, there has been a 50-fold increase in dollars invested in commodity index funds. In the first 55 days of 2008, speculators poured $55 billion into commodity markets, and by July, $318 billion was roiling the markets.”

“Any market where a $2,000 down payment will buy you a futures contract on a $1-million Treasury bill promises the customer action that can match any packed casino for electrifying excitement.”[4]

As has been well documented, rising commodity markets have enriched the few, but impoverished millions of people. Driven in part by higher fuel costs, global food prices are 36 percent above their levels a year ago and remain volatile, the World Bank argued in a recent report:

“A further 10 per cent increase in global prices could drive an additional 10 million people below the $1.25 extreme poverty line. A 30 per cent price hike could lead to 34 million more poor. This is in addition to the 44 million people who have been driven into poverty since last June as a result of the spikes. The World Bank estimates there are about 1.2 billion people living below the poverty line of US$1.25 a day.”

Lower commodity prices are central to any strategy for reducing global poverty. On 6 May, 2011 global commodity markets were subject to what the FT called an ‘epic rout’

“…the worst sell-off for many commodities since the collapse of Lehman Brothers and, in dollar terms, the biggest-ever for Brent crude.”

While these markets may well stabilise, and be talked up (and down) again, it daily becomes clear to even the most orthodox economists that, in the real world, the global economic ‘recovery’ is very weak indeed. Will there follow a collapse in index-traded commodity prices?

Furthermore, margin debt — the amount that speculators borrow for speculative purposes — is rising quickly, just as it did in advance of the 1929 stock market crash, the Nasdaq bubble and the subprime crash of 2006/7. Indeed, as the blogger, Cullen Roche of ‘Pragmatic Economist’ notes, margin debt is now at ‘manic levels’. Debit balances at margin accounts skyrocketed to $20.7 billion in February:

“Only two other times historically have we seen leverage rise so much so fast and both times it was during a manic phase – during the tech bubble of the late 1990s and the credit bubble just a short four years ago.”

These debit balances, as an anonymous player at an investment boutique notes:

“increase speculative volatility in things like oil, which goes from $40 to $150 to $50 to $130 over and over. Paper profits change accounts but the real economy is not theoretically affected, except that it is held hostage to this casino game of rapidly changing prices for basic materials and necessities that businesses and consumers use to make decisions. So the economy is in actuality disrupted by the casino, the casino creates no net wealth, and everyone is worse off as this charade continues.”

We’ve been here before. Akyüz argues that the post-2000 ‘swings in commodity markets show strong correlation with those in capital flows’ to developing and emerging markets (DEEs) and with it ‘the exchange rate of the dollar’. After rising constantly, both commodity prices and flows declined in 2008, when falling prices triggered the exit of capital from commodity-rich economies. Both recovered rapidly afterwards.

These factors are reinforcing with ‘greater force the macroeconomic imbalances and financial fragility in several DEEs….Imbalances that started with the subprime bubble but were interrupted by the Lehman collapse.’

Akyüz cautions that the continued boom in commodity prices could eventually cause rampant inflation in China, which could lead to a sizeable slowdown.

‘This, together with the global oversupply built during the boom, would bring down commodity prices, and the downturn would be aggravated by an exit of large sums of money from commodity futures. This would make investment in commodity-rich countries unviable and loans non-performing, leading to risk aversion, flight to safety and a reversal of capital flows to DEEs.’

The most vulnerable of these are countries in Latin America and Africa that have enjoyed the twin benefits of global liquidity and the boom in commodity prices. They could be hit twice – by falling capital flows and commodity prices, he argues. South East Asian economies are less vulnerable, because they have built up substantial current account surpluses and large stocks of reserves.

Akyüz concludes correctly that these unstable capital flows and commodity price booms show that ‘the international monetary and financial system needs urgent reforms’, but that ‘macroprudential regulations, as usually defined, would not be sufficient to contain the fragilities that capital flows can create’. Instead, controls over both inflows and outflows should be part of the arsenal of public policy, used as and when necessary and in areas and doses needed, rather than introduced as ad hoc, temporary measures.

And we do not have to re-invent the wheel. ‘The instruments are well known and many of them were widely used in the advanced economies during the 1960s and 1970s.’

For further discussion: reforms to the international financial architecture?

Should the following principles and proposed policies guide debate within the Labour Party on generating resources for international development?

- Empowering governments to respond to democratic mandates, by strengthening policy autonomy (which would imply changes to the IMF’s mandate/approach to support for its members [5] ) while restoring the finance sector to the role of servant to the global economy?

- Taming financial markets through the re-introduction of capital controls; regulation over the growth of credit; and the establishment of an International Clearing Agency, for a new currency regime consistent with keeping international trade and investment open to all nations on equal terms?

- As a corollary of the above, the primacy of low interest rates[i] – both to levels of investment and also to financial and ecological sustainability; and the need therefore for Labour to lead, through the IMF, a globally co-ordinated drive to lower interest rates – across the spectrum?

ChartSources: Bordo et al. (2001), Caprio et al. (2005), Kaminsky and Reinhart (1999), Obstfeld and Taylor (2004), and these authors. Notes: As with external debt crises, sample size includes all countries, out of a total of sixty six listed in Table 1 that were independent states in the given year. On the right scale, we updated our favorite index of capital mobility, admittedly arbitrary, but a concise summary of complicated forces. The smooth red line shows the judgmental index of the extent of capital mobility given by Obstfeld and Taylor (2003), backcast from 1800 to 1859 using their same design principle.

[1] “The three decades following World War II seem to have been a golden era of tranquillity in international capital markets, a fulfilment of the benediction ‘May you live in dull times’ … Sovereign defaults and liquidity crises were relatively rare.” Barry Eichengreen & Peter H. Lindert, The International Debt Crisis in Historical Perspective. 1991.

[2] For more on this see Eric Helleiner “States and the re-emergence of Global Finance: From Bretton Woods to the 1990s.” Cornell University, 1994.

[3] Prof Victoria Chick: speech to ‘banking summit’ sponsored by new economics foundation, 30 May, 2011. Published on PRIME (Policy Research in Macroeconomics).

[4] “Who Guards Whom at the Commodity Exchange? – Fortune July 28, 1980.” Reposted by CNN Money, 8th May 2011.

[5] See Yilmaz Akyuz “Financial instability and countercyclical policy.” UN Desa, 2000. “Fund programs have come to be built on the premise that a developing country should interpret every positive shock as temporary and thus refrain from using it as an opportunity for expansion, and every negative shock as permanent, thus adjusting to it by cutting growth and/or altering the domestic price structure. “

[i] “In my view the whole management of the domestic economy depends upon being free to have the appropriate rate of interest without reference to the rates prevailing elsewhere in the world. Capital control is a corollary to this.” John Maynard Keynes. Quoted in “Keynes’s theory of liquidity preference and his debt management and monetary policies” by Geoff Tily. Cambridge Journal of Economics, April, 2004.